Breaking down the UPI 30% Rule (#18)

Thoughts on the details, challenges, and implications of the cap on UPI volumes

The last month has been all glamour for the Unified Payment Interface (UPI). In the last week of October, to much anticipation, transactions on the system crossed two billion for the month - a number higher than the number of card transactions for the same period. This assumes even more significance when we consider that the UPI system launched only four years ago, while cards have existed through our entire lifetimes. A success that makes even institutions in the West feel envious.

But this news was dwarfed by another in the following week. On 5th November, NPCI issued a much-feared press release that aims to cap volume share of Third-Party App Providers (TPAPs) such as Google Pay and Walmart-backed PhonePe.

Feared, yes – but hardly a shock. There have been talks of capping UPI volumes for over a year. These were proposals for gradually limiting market share from 50% in the first year to 33% by the third. The plan was put on hold in November of last year. But not for long - as the talks resumed, only for whispers of a withdrawal to circle back again. Lobbying and speculations have been the norm for this while.

Now, finally that the regulation proposal has been issued, there is much to ponder and panic over. Unless there are reversions of the mandate or any relaxations therein, we can expect a market that was heading towards a duopoly to settle instead for a highly regulated oligopoly. There are several complications, some winners and some losers, of this regulation. I will elaborate on these later.

Before that, we dive deeper into the press release. The statement highlights two components, both interesting for varying reasons:

The cap of 30% will be calculated basis the total volume of transactions processed in UPI during the preceding three months (on a rolling basis).

The simple interpretation for this is that a third-party UPI provider is found to be violating the law only if the average volume share over the latest three months crosses the 30% mark. Banks, called the payment system providers, working at the back end will continue to notify NPCI of the monthly UPI transactions on their networks.

The rolling basis allows those found to be on the wrong side to push their numbers down and escape without consequences. At the same time, those ending substantially below the 30% mark can pull themselves up without much fear. It will be exciting and, maybe comical, to see how this criterion plays out.

The existing TPAPs exceeding the specified cap will have a period of two years from January 2021, to comply with the same in a phased manner.

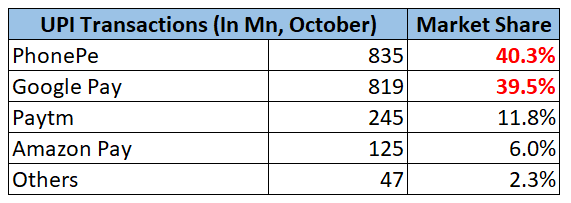

This defines the timeline for complying with the 30% rule. The table below shows the present share of UPI transactions (not volume) amongst major UPI providers:

Both PhonePe and Google Pay, given that they exceed the 30% share, will be allowed two years, i.e. till January 2023 to comply with the rule – while the others such as Paytm, Amazon Pay, Mobikwik, and the like will be required to follow the guidelines from January 2021 itself.

Why does NPCI care?

The rationale for putting these caps on third-party application providers is not exact. But I support a couple of popular theories that might explain this:

Local UPI applications for a local system

Distribute power to reduce dependence on one/two parties

Digital transactions are growing fast in India. Redseer expects digital payments growth at 27% CAGR over the next five years. And when India’s newest, brightest payment-system is growing at a speed that few anticipated – with thousands of merchants being onboarded every day – not many doubt that the government-backed UPI will be one of the key levers of this push.

This is where, when the government and NPCI, see two companies – largely foreign-owned (Google Pay and Walmart backed Phone-Pe) dominating the locally devised payment method – there are doubts. NPCI, on much push from RBI, even started seriously auditing data localisation for UPI providers last year. Although there have been concerns about the rigour of these audits.

Either way, the 30% rule - given this context - can be an attempt to push more local UPI application providers at the top. Or the bank-led UPI applications such as BHIM. This would be tough since most TRAPs lagging behind the top two also see large foreign influences. And the one waiting in line – WhatsApp Pay – does not fit the bill as well.

Perhaps the bigger fallacy to this thought is how the zero MDR and transaction fees (although NPCI is pushing for MDR to return), along with added costs of compliance through data localisation and audit norms are expected to even attract new UPI application providers.

More so then, the cap is simply a ploy to ensure that no single player has too much influence on UPI payments. The obvious benefit of this is to limit the systematic risks, that of the UPI system being dependent on only one or two third-party applications. This was increasingly becoming more plausible, but few still doubt the veracity of this concern.

Should NPCI be worried?

The lessons from China teach us the follies or foibles of a private-sector duopoly in payment systems. Much like Alipay (Alibaba) and WeChat Pay (Tencent), PhonePe and Google Pay have started to build closed-loop ecosystems around their UPI payments.

Recently, PhonePe became the largest platform for buying gold. And much less discussed, but PhonePe added tax-saving funds as a wealth management solution early this year too. Google Pay, unlike PhonePe, has stuck to payments but we see Google expanding its financial services elsewhere.

But maybe, NPCI is more concerned about a player with zero market share today.

WhatsApp Pay. The closest parallel to Tencent’s WeChat App the world will soon have. With a network of ~400Mn Indian consumers, a full-fledged rollout can ruffle UPI market shares in a few months. Interestingly, the go-ahead for WhatsApp Pay in India was given only a few minutes after NPCI issued the press release. A happy accident, perhaps.

But if we are to learn from the Chinese experience, we must note both the good and the bad. For one, the might of Alipay and WeChat Pay was crucial in digital payments inclusion of over 90% population of the country. At the same time, most of the innovations in payments (QR, wallets, online payments) were led by these two players. For all we know, the Chinese experience with payments would have been worse without the duopoly.

However, this is – as NPCI probably supports – a slippery slope. Early adopters of new technology do get an unfair advantage over others. And if a monopoly or a duopoly dominates UPI, NPCI essentially becomes a prisoner to the exploits of those leaders. A power game, if there was one. This is where NPCI, perhaps under the influence of the center, chose to take a stand.

How will this play out?

It is tricky to predict how this will progress. We have hardly any details on how the rule will be enforced. And more importantly, on whether it can be enforced. Can NPCI pre-determine the volume of transactions to push limits on application players or will it transfer that responsibility to the TRAPs themselves? Will quotas be distributed to application providers and will they prove anti-competitive?

To be fair to ourselves, there are just so many more questions than there are answers today.

Will NPCI moderate three-month volume shares in real-time? Daily? Weekly? Monthly? What are the penalties for a 30%+ share? What does an application do if they are seeing traction that would lead to high market share? What if your volumes grow at the same pace and the volumes of others drop – are you penalised for higher share then as well?

And on and on.

These are all questions we can speculate about, but will only know the answers to when NPCI comes clear. Regardless, we can hypothesize on the impact the law, if applied as stated, would have on the major stakeholders of the system: third-party application providers, users, and merchants.

UPI Third-Party App Providers

We must realise the awkwardness of the situation for UPI applications. In the payments industry, your margins are already extremely low. The success then more often than not depends on your ability to scale. Now, add to that the puzzling mandate to keep MDR or transaction fees to zero, and you are left with hardly any incentives to operate as a UPI application alone. For the providers, this meant an almost forced expansion into financial services such as insurance and wealth management to leverage their large payments user network, and earn on platform fees. These revenues justified the long-term strategy of PhonePe and Google Pay with UPI.

But now with the mandate to keep the UPI volume share down, the application providers are not only forced to expand into financial services but perhaps also onto other payment methods. We might see them pushing card transactions in-app even more through rewards or other behavioural tactics.

Moreover, the market earlier was defined by competition for UPI volumes. But with the forced ceiling on volume share, the fire for competing will burn less brightly. In fact, as is common to oligopoly markets with high regulation scrutiny, we might see Google Pay and PhonePe empathize with each other and indulge in tacit collusion. An agreement to share information on UPI volumes for each to maintain a ~30% share would not be surprising. All moves may be directed to maintain their power.

Thirdly, with scrutiny over the management of volume share within the 30% range and the mandatory auditing of data localisation norms, expect higher involvement and moderation by NPCI into UPI application businesses. Lastly, with the volumes so tightly managed, the application providers will have to invest heavily into forecast models, perhaps learning a thing or two from inventory management. Forecasting the pull of advertisement and marketing campaigns will be particularly challenging.

Consumers

For the UPI users, the implications will be unexpected. With limits on volumes, the users might have to switch to other platforms for UPI if the option is disabled on their primary choice application. Moreover, the rule might even be enforced by setting a limit on UPI transactions per user beforehand, affecting the ardent users UPI users the most. This would again force consumers, who earlier relied on one UPI application, to multi-home. For the consumers, this would mean a worse customer experience. And for the applications, this would weaken the loyalty of their customers, which they have paid heavy costs to build.

Merchants

We have discussed the huge expectations for digital payments growth in the country. A direct enabler of growing digital payments is onboarding new merchants to payments platforms. And for the UPI providers at the top, a sales team onboarding thousands of merchants every month was a day 1 strategy. But now with little incentive to grow volume share, and perhaps penalisation for the same, the efforts to sign up merchants at the same pace would be fewer.

For applications with lower volume shares or applications willing to build UPI platforms, the capacities and knowledge of merchant onboarding would be comparatively lower as well. All this points to the uneasy realisation that the regulation might impact the growth of digital payments in the country, which goes directly against the primary objective of NPCI.

It will be interesting what the think tanks at RBI make of this.

Final thoughts

The regulation has divided opinions already, more so against the regulator. The implementation and implications are both little understood today. But we can be sure that the move rakes of a fight against a single-party or a duopolistic market structure, which was certainly looking more plausible. The concerns of NPCI are likely drawn from the China experience and from a need to retain market influence. The introduction of WhatsApp Pay only adds to these concerns, and NPCI seems to have taken a strong stand to retain control.

With the costs of compliance and the zero-MDR, the incentives to push competition are hardly worthwhile. More so, the efforts to bring in New Umbrella Entities (NUE) were perhaps sufficient to foster a healthy competition. And much worse, the implications for the new 30% rule might be more unintended than imagined.

For third-party application providers, expansion into other payment methods and tacit collusion – as is common to oligopolistic markets – might be the outcomes. Higher moderation from NPCI and the need for building forecasting models are also possible hypotheses. For the consumers, forced multi-homing and a poorer experience will likely be the unwelcome consequences. Lastly, for the merchants, the push towards onboarding might weaken as players at the top adjust their volume shares. These are all possible outcomes that might eventually harm the market.

There are of course winners of the regulation such as Paytm, Amazon Pay, and even WhatsApp Pay, who would gain big in the short term. But eventually, capping the market appears more anti-competitive and ill-imagined. Importantly, we must also ask whether NPCI – a committee of member banks wherein each bank can build a competing UPI application – should even be allowed to set rules or market competition, being neither a regulator not a competition authority on paper.

For now, we can only trust and keep an eye on how RBI responds to the seemingly bureaucratic rule. It will, no doubt, be equally interesting how NPCI unpacks the implementation and how the UPI application providers respond. All points considered, this might possibly change the future of UPI in the country.

Other interesting reads on the topic:

On the thoughts on the impact of the UPI rule by Anand Raman in Mint

On the details of the NPCI 30% Cap by Harshit Rakheja in Inc42

If you have any views or feedback to share, feel free to add a response below or to share your thoughts with me over Linkedin. In case you feel your friends or family would be interested in reading about fintech or economics, feel free to share the blog with them as well. See you in a week or two!