Facebook's Payments Struggles and the Diem Dream (#32)

Facebook Credits, Pay, Libra to Diem, the New White Paper, Novi wallet and more

Welcome to the 32nd issue of the Unit Economics. The article today is a long-read on Facebook’s struggles with payments that started twelve years ago. I detail out the key developments over the decade-long timeline, and put particular focus on Diem and Facebook Pay. Feel free to reach out to me if you have any thoughts or questions on the topic!

P.S. The number of daily COVID cases in India are still 20% more than the cases at the peak of the first wave. If you want to help, please donate across verified organisations here.

Building a business is hard. Building one centred on payments only aggravates the feeling. Low margins, regulations, dealing with banks, price competition, and whatnot. And few understand this better than Facebook.

Facebook first forayed into payments twelve years ago. At the time, in 2009, large communities had already developed on Facebook for social games. The extent of the popularity of these games is hard to overstate. For instance, Zynga – the most popular of the game developers - had built a monthly active user base of 240 million on the backs of games such as FarmVille, Mafia Wars, Texas HoldEm. The population of the US was only a little more at 300 million at the time. Other statistics are similarly revealing: 40% of all the time spent on the social network was towards social games in 2010, 50% of Facebook logins were to specifically play games, and more than 20% of users had paid money for in-game benefits.

Facebook had all this data and more, and the opportunity for in-game commerce was obvious.

Enter: Facebook Credits

Facebook Credits was a virtual currency that allowed the purchase of in-game items initially. Imagine an extra cow for your farm in FarmVille. Slowly, as the Credits developed, there were speculations in the developer community of Facebook’s aggressive plan to make Credits the sole virtual currency on the platform. That is, no other method of payment could be used to buy any in-app item on Facebook. This turned partly true soon, and in April 2010, Facebook mandated that the Credits be the only payment option for social games on the site and asked developers to make changes accordingly within the year.

The idea also had an app-store like overtone. That is, through Credits, Facebook would take a 30% cut. For Zynga, which was expected to make more than $500 Mn from virtual goods in 2010, the rule meant a $150 Mn platform fees. But for Facebook, given the almost triple-digit growth in in-game purchases, this was a billion-dollar revenue opportunity.

Credits did not remain limited to games for long. By early 2011, Facebook users could use their Credits to rent movies and to purchase gift cards for friends and family from major retailers such as Tesco, Target, and Walmart. As the popularity gained, applications started offering Credits as incentives for downloads and some newsletters did the same for subscriptions.

All these were small steps to make Credits a “safe and secure way” for online payments, as Facebook called it. At this point, users could purchase Credits in up to 15 currencies, and exchange 10 Credits for $1, through a multitude of payment methods – credit cards, PayPal, and even prepaid cards. Facebook even incentivized higher purchases through a higher-credits-per-dollar ratio for larger exchange amounts.

In Apr-2011, Facebook launched Deals, where users could share discounts and vouchers with friends, see when someone in their circle purchases something, and find offers that their friends are interested in. This put Facebook in direct competition with the likes of Groupon and LivingSocial, but also provided a big use case for Credits which could then be used to purchase vouchers for real goods and services through Deals.

We can see that there was a lot to be excited about. Facebook even launched a separate subsidiary to handle payments in Mar-2011 – Facebook Payments Inc. But within the next year, by Jun-2012, Facebook Credits was shut down.

Anti-climactic, obviously – but why did it happen?

While Facebook launched Credits, games had also increasingly developed their own in-game virtual currencies. Moreover, Credits limited the ability to price differentiate the users on a market-by-market basis, which theoretically reduced the possible surplus for applications. And the 30% commission was the icing. Overall, the developers felt that Credits were restrictive and limited the potential innovation. In short, they were not pleased.

This abruptly ended Facebook’s first dive into payments. And by Sept-2012, Facebook converted all the virtual Credits into local currencies and introduced Subscriptions instead as a way to monetize through recurring revenues from any games or applications on the network.

The platform fee from processing payments was a big drawdown from the ambitious Credits. So, where did it go next?

Money Transfer, P2P, and WhatsApp

Facebook did not come up with anything big in payments for a couple of years. There were speculations in early-2014, however, of Facebook working on a Europe-wide money transfer service, similar to what a Western Union or Wise offers. Remittances are a complicated but high-margin business. And Facebook’s extensive Money Services Business (MSB) licenses, and reach on either side of the transfer put it in a good position. But nothing came off these suppositions, and instead, Facebook launched a no-cost Peer-to-Peer payments transfer service – similar to what a Venmo or Cash offers – through Messenger in 2015.

The idea of offering a no-cost P2P payments service was more to lock consumers on its platform, a platform that had grown increasingly rich and dependent on advertising revenues. The rationale was that consumers were already doing conversations on trips, bills, and payments on Messenger, so why should they have to open a different application to do the payment.

And in between the speculations and the P2P offering, there was the $19 Bn acquisition of WhatsApp in late-2014. At the time, there were guesses on how Facebook will monetize WhatsApp, and payments were one of the reasons widely quoted - especially with the leaks on P2P, the hiring of PayPal President David Marcus as the VP of “Messaging Products”, and the speculations on money transfer services.

If we follow the logic for the Messenger payments, the WhatsApp acquisition is not too different. The distribution and the possibility of converting in-app conversations related to payments to actual payments were equally large, if not more, with WhatsApp.

Finally, after almost seven years, we are seeing signs of progress for WhatsApp Pay in both Brazil and India. The usage, unfortunately, is still limited to P2P in both regions, but once it receives the greenlight for merchant payments and restrictions on the scale are lowered– the 500 Mn+ users of WhatsApp should allow Facebook to diversify away from advertisements. (I had previously written on WhatsApp Pay here)

The acquisition of WhatsApp and the launch of Messenger payments were definite signals that Facebook imagined a bigger role for payments in the company. Over the next seven years though, Facebook would go a few steps further. It would join and, de-facto, head the Diem Association (earlier known as the Libra Association), launch Facebook Pay, ideate Novi wallet (earlier known as Calibra), and set-up Facebook Financial.

I will briefly go through Facebook Pay and Facebook Financial, and then discuss the more interesting developments on the Diem/Libra Association and Novi wallet in detail.

Facebook Pay and Facebook Financial

As the trimmed down P2P payments through Messenger provided learnings for Facebook on how to combine messaging and payments, which will undoubtedly be crucial with WhatsApp, Facebook upgraded the payment facilities within the eco-system through Facebook Pay.

Launched in Nov-2019, Facebook Pay is meant to be used across Facebook, Instagram, Messenger, and WhatsApp, with the functionality varying across geographies. The following broadly capture the method of payments and the types of use cases it presently supports:

Form Factors - Credit cards, Debit cards, Wallets

Use Cases - Facebook: shop on Facebook Marketplace, donate to fundraisers on the network, and purchase games, tickets to events, and premium content on Facebook Watch; Messenger: split bills with friends; Instagram: checkout from brand pages without leaving the app, and donate to Instagram fundraisers; WhatsApp: send to and receive money from your peers.

We see that the functions are rather limited across platforms right now, with no P2M support on WhatsApp and no creator or micro-payments on Instagram (although it did launch Fan Subscriptions for creator payments). Moreover, a look through the available facilities across countries will tell one that Instagram, WhatsApp, and Messenger stay largely untouched by Facebook Pay even after 21 months.

There is limited information in the public domain on how Facebook is thinking about Pay, and neither are there any references in the earnings call or the 10-K. However, I would hypothesize that unlocking P2M payments on WhatsApp, adding local and region-specific payment methods on the platform, and a more sophisticated Shops or Marketplace experience on Facebook and Instagram would go a long way in solving some of the issues. Mark Zuckerberg and a few others have briefly mentioned the focus on commerce in a few interviews. For all we know, at this point, it might all simply be a waiting game.

Another interesting development relevant to Facebook Pay has been the introduction of Financial Financial, called F2 internally, in Aug-2020. Headed by David Marcus, the team will be responsible for heading all payment initiatives for Facebook. And as the name suggests, the services might extend beyond payments as well. As far as conjectures go, one of the risks highlighted in Facebook’s K-10 gives weight to the assertion: Depending on how our Payments product evolves, we may also be subject to other laws and regulations including those governing gambling, banking, and lending. Make of that what you may.

Libra Association

In May-2018, David Marcus – then part of Facebook Messaging – was also asked to head a new blockchain division at Facebook. He had previously been the President at PayPal and had served on the Board for Coinbase, so he had the requisite payments experience and network. But it was not until word from Facebook’s new crypto developers spread that the tech media, in late-2018, would confirm that Facebook was working on some cryptocurrency.

The earlier rumours signalled that the organisation was working on building a cryptocurrency that would allow money transfers on WhatsApp, with a great focus on remittances in India. A textbook example of optimism.

For the pragmatic, the lack of clarity continued. But things got more clear in 2019. In Feb, Facebook acquired Chainspace, which was building a decentralized “smart contracts” system that could facilitate payments through blockchain technology, with one of their goals as improving the speed of transactions. The speed of transactions is a key metric formally measured through the number of transactions that the system can process per second.

In May-2019, reports indicated that Facebook was working on a stablecoin, and had the support of Visa and Mastercard. And in June, finally, Facebook officially introduced Libra to the world. Libra cryptocurrency was ideated as a stablecoin that would be tied to a basket of currencies and which would allow one to buy or exchange money at near-zero fees. The coins would be stored in either third-party wallets or Calibra, the wallet that was being developed by Facebook and the wallet would integrate with WhatsApp, Messenger, and other apps in the Facebook ecosystem.

The Libra Association, as opposed to the conventional thought, was not to be headed by a single organization but was instead planned to be a consortium of many members, which included Visa, Uber, Mastercard, Andressen Horowitz, Stripe, and 23 others. And Facebook, similar to others, would have a single vote in its governance and no outsized influence.

The goal of the association was to enable a single global currency and financial infrastructure that would be simple to set-up, accessible by the unbanked, efficient with lower fees – as opposed to Bitcoin and Ethereum, and last longer through decentralisation. Audacious, to say the least. The Association highlighted that an average person pays 7% in fees that send money abroad and wanted to provide a simpler way to convert the currency to Libra and then to transfer it across geographies. Further, the members would earn through interest on the money that users cash in and that is kept asreserve to maintain Libra’s position as a stablecoin. These were only the first steps, however. A lot of work had to be done to improve the chinks in its blockchain technology.

Technology was not the only challenge, however. Within a few weeks of the official Libra announcement, U.S. Senate Banking Committee had asked Libra Association to halt all development efforts, and kept a hearing for the same in July. The G7 nations had formed a task force to evaluate Libra. Several lawmakers and the privacy and consumer watchdog asked Libra to be halted. Federal Reserve chair, Jerome Powell, questioned Libra’s potential for money laundering and its impact on financial stability. And a month later, the EU had raised an antitrust probe.

Fair to say that Libra did not have a lot going for it.

Moreover, with the rising pressure, several prominent members of the group left the Association. These included Visa, Mastercard, PayPal, eBay, Stripe, among two others. The launch date, planned in 2020, became a non-event amid this chaos.

However, the negotiations with the regulators continued. Libra Association swore to abide by all regulatory necessities, did strategic hires, and made forced changes to its model. The new vision was detailed in the revamped white paper that was released on Apr-20. I will cover the important changes to the white paper in detail.

Single-Currency Stablecoins and Other Changes

The earlier Libra model ideated building a single multi-currency stablecoin (≋LBR) that was to be backed by five fiat currencies – US Dollar, Euro, Yen, British Pound, and Singapore Dollar – in varying proportions. Given the scale of the members that were part of the association, financial institutions grew concerned that if the scale of Libra were to become large enough, it could potentially challenge the ability of individual central banks to manage their currencies and of governments to track foreign trade. Moreover, financial institutions simply would not want a currency that includes anything other than their national currency to be used significantly for domestic transactions.

In the new model, the association would instead introduce multiple single-currency stablecoins, each backed by the domestic fiat currency. For example, LibraUSD or ≋USD would be backed by USD reserve, and LibraEUR or ≋EUR would be backed by EUR reserve. The single-currency stablecoins will be minted and burned based on market demand for that specific market. And the 1:1 backing will ensure that the approach will not result in the creation of a new net money.

The multi-currency coin (≋LBR) would still exist, but its flexibility would be severely limited by the fact that it would be backed by the new single stablecoins and not the fiat currencies held by the bank. Essentially, it would act as a digital composite of the single-currency stablecoins and be used primarily in countries whose currencies do not have a single-currency stablecoin. Further, while not acting as a separate asset, the paper states that ≋LBR would still be an efficient cross-border settlement coin as well as a neutral, low-volatility option for people and businesses. In this case, people and businesses would simply convert the ≋LBR they receive into local currency to spend on goods and services through third-party financial service providers.

This switch to single-currency stablecoins was the single most fundamental change to the model. There were, however, three other significant changes.

I. Staying Permissioned

The earlier white paper imagined the transition from a permissioned to a permissionless network within five years, wherein unknown members in the network could act as validator nodes, i.e. be responsible for maintaining the current state of the blockchain. However, concerns were raised that this could challenge the ability of the Association to guarantee that the compliance permissions would not be compromised.

To this effect, the new white paper outlines that although new members can run independent validator nodes, they would be required to go through thorough due diligence, incl. sharing basic information, proving technical capability, showing past performance, and financially supporting the association. This ensures that there would be no ‘unknown’ counterparties to the team, with the blockchain effectively acting as a more spread-out centralized system, with limits on how the ledger is distributed.

II. Stricter Compliance Framework

Based on the conversations with the regulators, the Association has made several changes to improve network-wide security. This involves the establishment of a Financial Intelligence Function (FIU-function) to help support and uphold operating standards for network participants, and building a new roadmap that will be more compliant with the recommendations of the Financial Action Task Force (FATF).

Additionally, “unhosted wallets” will be subject to balance and transaction limits until the compliance framework says otherwise. Initially then, the network will only be available to two participants: Designated Dealers, and Virtual Asset Service Providers (VASPS, incl. exchanges and custodian wallets) that have completed a certification process approved by the Association.

III. Redesigning the Reserve Framework

In the earlier white paper, the Association committed to the full backing of the reserve, i.e. reserves in the form of cash and cash equivalents and very short-term government securities will be maintained in equal value to the face value of the Libra Coins in circulation. The new paper maintains the commitment to full backing, but to counter external risks to the system (for example, rapid changes in interest rate impacting the value of government securities), the Reserve will be endowed with a loss-absorbing capital buffer that protects the payment system from credit, market, and operational risks. Moreover, the loss arising from negative yields on the assets would be borne by the revenues earned from fees and the interest of members.

The paper also highlights how the Reserve would function in stressed scenarios, such as when it is unable to convert the very short-term government securities in the Reserve into cash fast enough, ensuring that emergency operations are prepared for in advance.

The Libra Association went through a rebranding on 1st Dec 2020, transitioning to ‘Diem Association’ in the hope for change in fortunes to the payment system. A few months ago, Facebook’s Calibra wallet had undergone a similar exercise, branding as ‘Novi’.

Facebook’s Novi Wallet

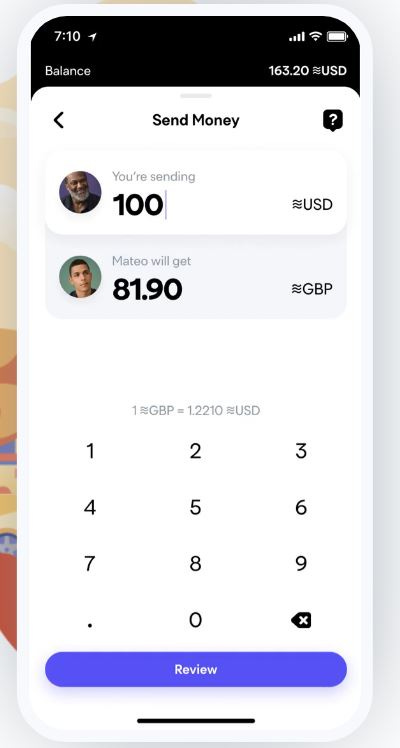

Facebook continues to play the role of a sponsor and flagbearer for the Diem Association. However, on paper, its primary part is to build and distribute Novi – a digital wallet that can be used to hold the digital currencies from the Libra ecosystem. Novi has multiple parallels to the earlier discussed Facebook Pay, with the ability to integrate to Messenger and WhatsApp, while also acting as a standalone application.

The verification in Novi will be through government-issued ID, and given that Facebook will draw revenues from interest and fees on reserves, the charges to add, send, or receive money through Novi will be low. Additionally, the application will automatically convert local currency into the relevant Diem currency and allow transfers anywhere in the world with a few taps. There are likely to be more bigger complications on how the multiple currencies interact in the wallet, but we will have to wait for the launch to see the complete picture.

What is next for Diem and Facebook?

Few companies have battled as much as Facebook to build a payments business. But given the developments we have seen over the last two years – the introduction of Facebook Pay, the launch of WhatsApp Pay, and the development of a more sophisticated Diem Association and Novi wallet – there are reasons to be optimistic.

The focus for Facebook Pay and WhatsApp Pay will likely remain on exploring more commerce-specific use cases, and on slowly rolling out payments across all four applications. As for Diem and Novi, the following are likely to be important considerations:

The testing phase in Jan-2021 showed that the Diem network operated at a throughput of 5 transactions per second (tps), which was less than half of that of Ethereum (15 tps) and significantly lower than of Visa or Mastercard (24,000 tps). These numbers signal an obvious need for Diem to work on improving its technical capacities.

Given the new single-currency stablecoin structure of Diem, the wallet would have an added advantage of directly integrating central bank digital currencies (CBDCs), removing the effort required to build new wallets or for Libra to hold reserves. The integration of CBDCs with Novi and other certified wallets will be an important point of discussion.

The new model would equally add complexity for wallets, merchants, and exchanges to handle multiple digital stablecoins. The approach for Wallets on how they handle cross-currency use cases will have huge implications on the regulatory response and customer experience.

The Association will continue to expand its members strategically to bring in greater geographic distribution and diversity. It will be interesting to see what institutions from APAC and Africa, if any, join the existing members.

Lastly, the rollout of the payment system will follow a phased plan, especially with bottlenecks on transaction throughput and regulatory hurdles on attaining money transmitter licenses in different countries. If anything, the number of stakeholders and the policy of equal vote in Diem Association can make such policy decisions time-consuming and filled with inefficient trade-offs.

Considering it all, as consumers – and given the issues of remittances - we should feel hopeful, if anything, for what Diem might end up becoming.

If you have any views or feedback to share, feel free to add a response below or to share your thoughts with me over Linkedin. In case you feel your friends or family would be interested in reading about fintech or economics, feel free to share the blog with them as well. See you in a couple of weeks!