Fino: A Distribution Powerhouse (#42)

How Fino's large merchant, correspondent network, and the Emerging India focus make it stand out

Welcome to the 42nd issue of Unit Economics. For today’s issue, I dive into the operations of the Fino Payments Bank and argue why more people should be talking about it despite the IPO. Dive in!

Fino is not the first name you think of when you think of payments or banks. An IPO listing should have changed that for some. But even in a seller’s market, Fino Payments Bank got listed at a discount of 5% on Friday. This, I assume, is partly down to how little the company is known in an industry that carries some of the noisier heavyweights. Competing with the hype of Zomato and Nykaa (FSN) for retail and institutional pockets wouldn’t have been easy either.

Regardless, Fino has built a business exciting enough to command great attention. And a dive into its draft red herring prospectus (DRHP) reveals as much.

So, what does Fino do?

Fino PayTech Limited, of which Fino Payments Bank is a 100% subsidiary, began operations long back in 2007 and had since provided remittances (domestic) and Business Correspondent (BC) banking services to a host of financial institutions. In 2015, however, RBI granted Fino – and ten others – an in-principle approval to set up a payments bank, and in April ‘17, the final approval was granted.

This allowed Fino Payments Bank to commence operations in June ’17. But, as the regulations dictated, with a rather limited scope of activities. The cap on deposit balances of INR 1 Lakh and the inability to lend were particularly restricting for payments banks. The stringent regulations and a competitive environment meant that more than half of those with RBI approvals either went defunct or did not begin operations (wrote earlier here).

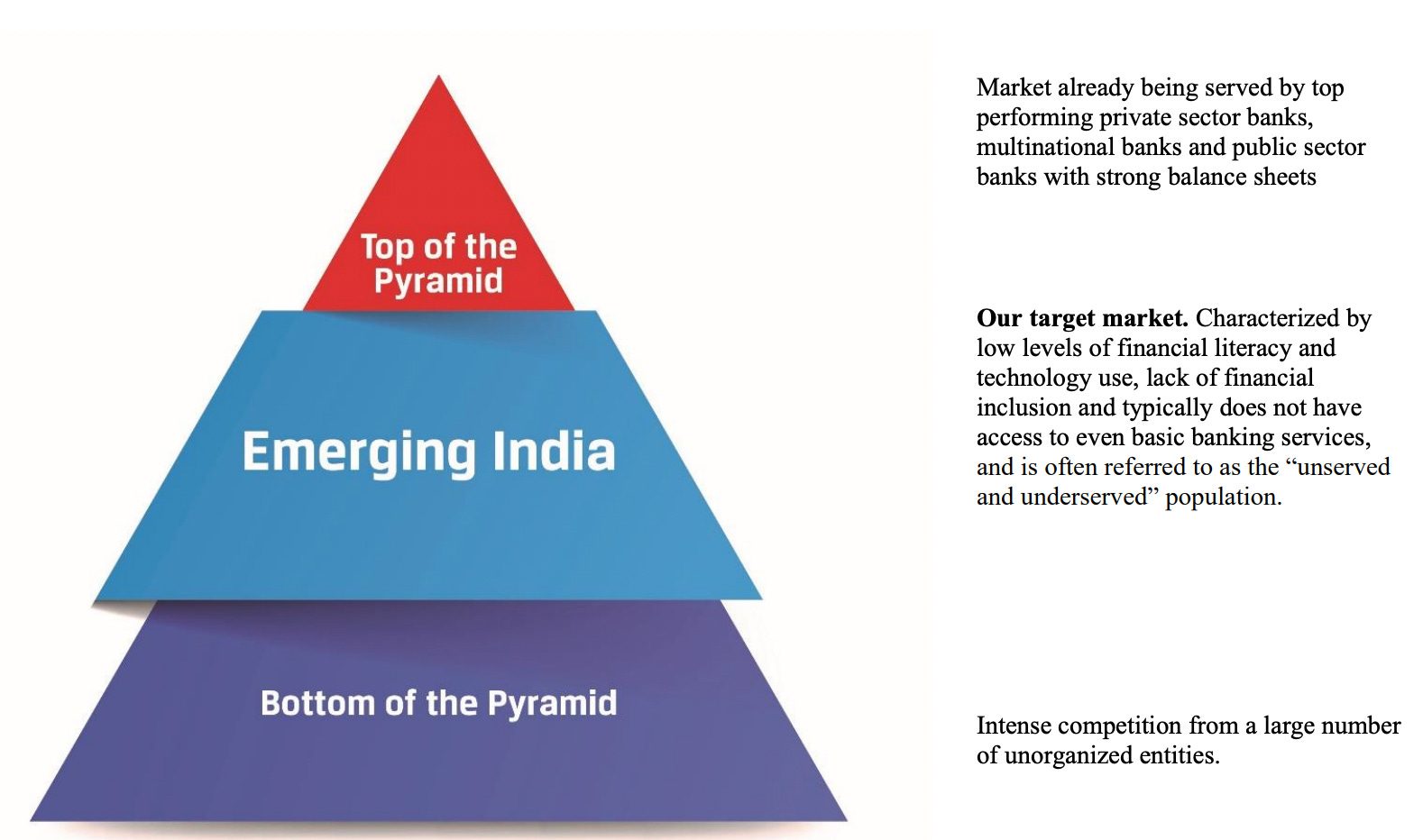

For Fino, however, the prior experience of providing remittances and BC banking services to Emerging India (see below) segment came in quite handy. Why? Because the need for a low-balance bank account is felt most by a segment that is capable but often overlooked by the traditional banks.

Moreover, Fino’s business model has traditionally relied on building a strong merchant and correspondent network. And when combined with the experience in distributing to the target group, the distribution expertise acted as the perfect foil to leverage the payments bank license.

This approach is formalized by Fino through its DTP (Distribution, Technology, Partnerships) framework. The framework suggests that Fino’s significant time and capital investment to develop service capabilities and scale have enforced network effects on its platform that are difficult to replicate for the competitors.

These principles, and the competition from the likes of Paytm and Airtel, have pushed Fino to significantly ramp up its operations lately. And in the four years since, the result is a ~642K strong merchant network and a professed presence in over 94%(!) of the country’s districts by Mar ’21. The urgency is also highlighted in an almost 3X transaction growth - from 154.02 Mn to 434.96 Mn - over the last two years. In the same period, the company’s income has more than doubled from INR 3,519.69 Mn to INR 7,707.72 Mn, wherein 97% of the income continues to be driven by transaction fees or merchant commissions and only 3% from interest.

Understanding Fino’s Products

Over time, Fino has built a portfolio of complementary products and services for its target group that matches or surpasses the offerings of direct competitors.

The company boasts about developing, deploying, and controlling the end-to-end operations of all the mentioned products. In addition, its network of merchants and BCs cross-sell a suite of third-party products, such as gold loans and insurance, where the focus essentially turns from B2C to B2B2C.

To understand how Fino sells, it helps to investigate how the distribution ticks before diving into the products.

As of June ’21, the bank had onboarded 724,671 merchants on the platform. These merchants are typically located in tier-2 and tier-3 cities and bear the majority of the capital expenditure costs of micro-ATMs or AePS devices, allowing Fino to operate with an asset-light model. Fino solves for merchant discovery for users through the Cash Bazaar feature in its retail application, BPay.

Fino makes it convenient for merchants to carry out banking and payments activities for its customers through its ‘Fino Mitra’ application. The application allows merchants to onboard CASA customers, carry out e-KYC, issue debit cards, or perform cash management or money transfer operations. In FY21, Fino added ~197K active users to the app and oversaw a transaction throughput of INR 49,287 Mn.

The company also has approximately 17,430 business correspondents (BCs), who act as retail agents on behalf of other banks (Union Bank of India, ICICI Bank, etc.) that Fino has commercial partnerships with. The BCs are mostly foot soldiers equipped with a handheld device for carrying out banking activities and a UIDAI compliant biometric reader for authentication.

Additionally, the company operates 54 branches and 143 customer service points (CSPs), which offer a standardized and complete banking experience to merchants and Fino’s customers.

The distribution focus is obvious from the above points. But what do the merchants and correspondents sell?

Micro-ATMs and Aadhar-enabled Payment Systems

Micro-ATMs are POS devices that require mobile or internet connections and that can be used to deposit or withdraw cash, check account balances, or request balance statements. Moreover, Fino uses the Micro-ATMs to allow transactions through “own” or third-party financial services entities, wherein the third-party API partners require Fino’s bank infrastructure to complete transactions, incl. end-to-end domestic money transfers.

Fino caters to 45 such API or third-party partners through micro-ATMs and generates an interchange commission of 0.5% of the transaction amount or INR 15, whichever is lower, for own and partner transactions. This commission, however, is split between merchants and Fino for “own” transactions and shared with API partners for third-party transactions.

As of Aug ’21, Fino has a market share of 51% of the total micro-ATMs deployed in the country, which validates its presence in the more local corners of the country.

The numbers show an overwhelming 8X increase in transacting merchants and volume of transactions over the last two years and portray a huge opportunity to increase penetration of ATMs in rural areas.

The trend is similar for Aadhar-enabled Payment Systems (AePS), which operate on a bank-led model and use Aadhar for identification of accounts and authentication of transactions. Customers can use AePS to deposit or withdraw cash, enquire about account balances, or perform Aadhar-to-Aadhar money transfers. The revenue model for AePs is similar to the one for micro-ATMs and so is the trend in adoption (see below).

Research by NPCI and CRISIL suggests an expected CAGR in AePS volumes of 31% for FY21 to FY25, likely to be driven by higher business correspondent penetration, new transaction use cases, and network effects in the rural areas for ATM usage.

My view is that the micro-ATM and AePS segment should remain a stronghold of the Fino Payments Bank business, and a big sell for India’s financial inclusion goals.

Domestic money transfers (Remittances)

For Fino, remittances are largely domestic money transfers from migrants to their homes in other states/regions. These transfers are carried out through merchants, BCs, or at branches or CSPs. Fino allows customers to process transactions through the IMPS and NEFT facilities and earns a percentage of the transaction value for each such transfer.

Two takeaways from the numbers:

Fino earns a marginally higher commission (0.91%) on “own” remittances versus the third-party or “API” remittances (0.86%).

The remittances product was the most impacted due to COVID-19 restrictions since the migrant population returned to their home states or regions, resulting in the value of transactions falling by ~28% YoY. As migrants get back to work, the remittances are likely to pick up the pace – although it does leave Fino exposed to considerable risk.

Current and Savings Accounts (CASA)

Fino presently allows customers to choose from amongst two current accounts or five savings accounts on its website and mobile banking application, BPay. The accounts can be used with debit cards and for functions such as UPI transactions, bill payments, money transfers, and other usual banking activities.

Fino earns income on CASA through either (a) annual subscription fee applicable on certain savings accounts, (b) fee when a customer is unable to maintain the required account balances, (c) fund transfers from CASA accounts, (d) fee on cash deposits and withdrawals, or (e) misc. fee for SMS alerts, account statements, or other banking services.

The CASA accounts drew an average annual income of INR 231.35 per account, and the growth in deposits of more than 5X in two years correlates directly to the transaction growth over micro-ATMs. Also, although Fino has ~2.57 Mn user accounts, 1.78 Mn of those were active in FY21 – implying that a healthy 69.3% of the portfolio was “engaged” in FY21.

Lastly, you would note that the company’s subscription-based CASAs are an interesting bet. These accounts, which make up over 70% of those active, were floated due to the insight that consumers distrust the transaction-linked fees. For such subscription accounts, Fino waives off the transaction-linked fees up to a certain amount and instead relies on the annual fees for income, giving weight to the customer-centric muscle at the bank.

Debit Cards

Fino offers customers either a classic or platinum Rupay debit card that is accepted across POS devices, online platforms, and ATMs throughout the country. The debit cards earn Fino revenue largely through the one-time issuance or annual maintenance fees. The transaction fee only kicks in when the amount being transacted is over micro-ATMs and exceeds the “free” limits.

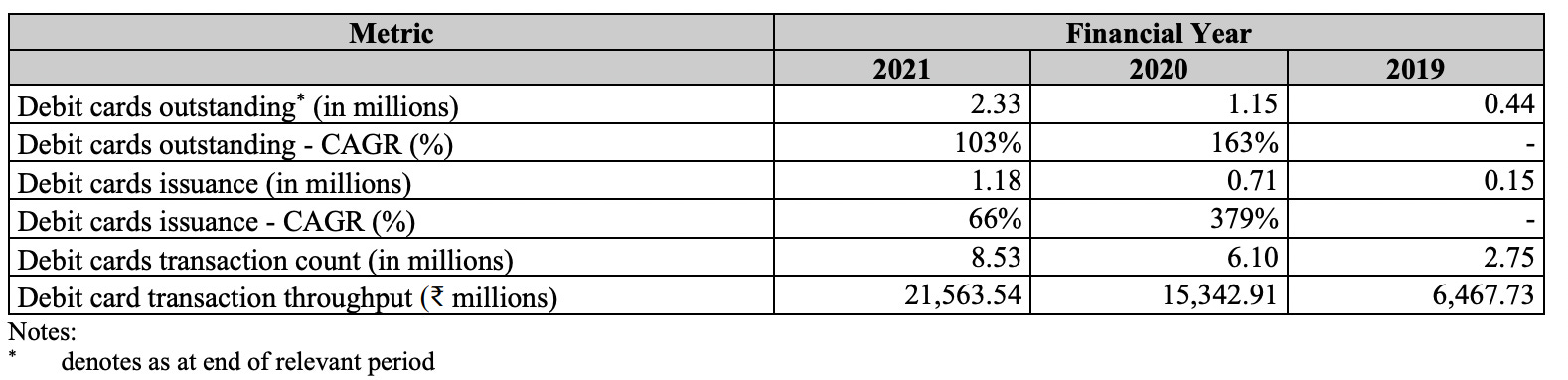

The company has seen an over 100% growth in the issuance of debit cards, although from a low base. Fino is expected to continue the growth trajectory for debit cards issuance and transactions in the tier-2 and 3 cities, where it faces low competition, and would benefit by migrating users to use cards for more use cases.

Cash Management Services (CMS)

Fino also offers cash collection and payments services to help digitize cash for clients who handle significant cash volumes. The process of collection is performed at the allocated physical locations, wherein the customers can deposit the cash and receive SMS or confirmation over the live dashboard of the acceptance and digitized amount. The service also involves the clients redirecting their customers to make the EMI payments on the Fino portal, of which Fino takes a commission and forwards the rest of the proceeds to the client.

As of FY21, Fino had 85 CMS clients wherein an average client contributed ~INR 1400 Mn in annual throughput. Going ahead, the company is bullish that many MFIs and NBFCs would accept payments through CMS providers, especially in the semi-urban and rural segments that lack the bank branches for accepting fees/repayments.

BC Banking

Fino derived an income of INR 1512.15 Mn in FY21 from the BC services that it provided on behalf of other banks. The revenue is largely on account of transaction commissions for services similar to those that Fino carries on its own platform.

Other Products

Given that the company cannot offer credit products as per the restrictions of the RBI license, Fino has smartly diversified its revenue streams by leveraging its distribution to cross-sell third-party products. The list of such products it offers is as follows:

Gold Loans: cash loans offered against the gold jewellery of customers. Fino entered into an agreement with an NBFC to cross-sell such loans via its network of BCs and earned income amounting to INR 102.69 Mn in FY21 in commissions.

Insurances: offers general, life, and health insurance as a corporate agent through partnerships with ICICI, Reliance, and Exide. In FY21, Fino’s network sold over 80K policies and earned it a commission of INR 9.55 Mn.

Bill Payments and Recharge: Fino operates a BB-POU under the NPCI’s Bharat Bill Payment System (BBPS) and allows customers to pay bills for utilities, municipal tax, mobile postpaid, and landline. The company earned a total income of INR 10.45 Mn through the provision of such services.

FASTags: charges flat INR 99 for each FASTag issued, and an interchange of 1.5% for every toll transaction. This is a high-margin product, but sees limited volumes in the semi-urban or rural areas and earned Fino revenues of only INR 0.48 Mn in FY21.

NFC Prepaid Cards: the touchpoints also offer users prepaid cards in association with City Cash. These are contactless smart cards used primarily for transit, such as for buses, that assist the state road corporations with contactless ticketing. Fino has cumulatively sold over 3 Mn such cards (more than its own debit cards). And the prepaid cards earned the bank a total convenience fee of only INR 0.87 Mn in FY21, wherein the income was adversely impacted due to COVID restrictions.

Business Loans: Fino also cross-sells working capital and business loans to its network of merchants and BCs through a partnership with third-party lenders. These loans are not available to Fino’s retail customers. In FY21, the bank earned a commission income of INR 0.67 Mn on account of these loans. With the growth in the number of merchants on the platform, the commissions from business loans should see a parallel increase.

The bank plans to launch a slew of new products, dependent on RBI approval, within the next year and benefits from the strong focus on the Emerging India target group. The money raised from the IPO should allow Fino to invest in technology infrastructure and personnel as well, and keep the investors happy with the top-line growth.

These declarations sound hunky-dory for Fino Payments Bank, but there still exist sufficient business and regulatory challenges to worry the investors.

While Fino is second amongst Payments Banks in terms of volumes, it is a distant second and processes only a fifth of the transactions that Paytm Payments Bank does. The bigger pockets and the merchant network of the likes of Paytm, Airtel are definite threats to the market share of Fino, even if it gets the SFB approval. This competition from the larger fintech players also makes it tough for Fino to equally access the private or public debt and equity markets.

Payments Banks have long been declared walking dead by the fintech community due to their inability to make big splashes, and the stringent regulations along with regular auditing from RBI are potential regulatory concerns.

The focus on profitability for the bank and the public market pressure that accompanies an IPO is likely to be a deterrent for Fino to maintain a high top-line growth rate.

Fino also faces legal proceedings against the bank for sums amounting to INR 48 Mn, with one from HDFC Bank on account of irregularities in their commercial agreement. A business model that has to rely on third-party partnerships for credit or insurance products faces considerable risks for more such litigations.

Lastly, certain product segments – remittances in particular – have been adversely impacted by COVID-19 and are yet to get back to normal levels. Fortunately, the other segments are seeing considerable growth to override the fall in the few, but this remains another big business risk.

Final few thoughts on Fino Payments Bank

The definition for Fino stands in stark contrast to most technology businesses of the day. The management of Fino has built an incredible distribution-heavy and asset-light payments bank that earns entirely through service and transaction fees. This is despite the regulatory restrictions, and with consistent profits for the last six quarters.

While there are some concerns as highlighted earlier, I believe that Fino Payments Bank’s (a) clear focus on the Emerging India segment, (b) stronghold on the infrastructure for banking and payments activities through Micro-ATMs and AePS technology in the remotest corners, and (c) the large merchant and BC network are substantial moats that should hold it in good stead for the long term. What remains to be seen is how Fino evolves if it gets the SFB license that would allow it to lend, and how it manages the expectations of high growth in the top-line along with a positive bottom-line.

Given the promising outlook of the majority of Fino’s products, if it had not already IPO’ed, I wonder if Fino Payments Bank would have been a top target for acquisition for the larger sharks because of the company’s relatively small size, effective management, and the fact that it does well in areas what few others do.

Moreover, with a fee and commission-based model, it might be unjustified to call Fino a bank. Instead, it is as much a technology business as a PhonePe or Paytm, and there is every reason for it to be valued as such. The prospectus validates this by highlighting the company’s almost 5X jump in technology infrastructure expenses from INR 139.33 Mn to INR 669.30 Mn in the last two fiscal years.

Lastly, Fino Payments Bank appears to be a business with clear strengths and focus areas. It is also one of the few businesses that are constantly delivering on their vision by smartly and profitably solving for financial inclusion.

If what appears is true, there is every reason to root for Fino Payments Bank’s success.

If you have any views or feedback to share on the topic, feel free to add a response below or to share your thoughts with me over Linkedin. In case you feel your friends or family would be interested in reading about payments, feel free to share the blog with them as well. See you in a couple of weeks!