How TransferWise beat Banks at their own game (#23)

On TransferWise's story, mission, products, profitability, and the road ahead (incl. IPO)

Building a business is tough as it is. If it is one in the payments industry, it only gets tougher. You scramble for margins that are thinner than anything you would hear on Shark Tank. And suddenly, digits after the dot gain relevance. Scale becomes a necessity, not an option.

Add to that a business that competes directly against something that banks have done all along. And done so quite profitably. Considering all this, the chances of success are hardly great.

But against these odds, TransferWise has challenged and built a successful platform for sending money abroad. The clarity of the purpose and the inch-perfect execution has allowed the business to grow to 10Mn+ users and a valuation of $5-10Bn today.

In this write-up, I dive deeper into how exactly they did that!

TransferWise: A cheaper, faster way to send money abroad

Taavet Hinrikus and Kristo Käärmann were both Estonians but had settled in London for work. Taavet, incredibly, was the first employee at Skype while Kristo was working as a financial consultant at Deloitte.

Note that the national currency for Estonia is Euro, while Britain’s is Pound Sterling.

Skype would pay Taavet in Euros, and he would convert the money to Pounds to pay bills in London. Kristo, on the other hand, would receive Pounds from Deloitte but had a hefty mortgage to pay in Euros back home. This meant that they had to go through the painful process of currency conversion frequently. Painful because Taavet was losing ~5% for every such transfer and Kristo shared the same plight.

Smartly enough, they formed a private arrangement to work around this. Taavet would deposit the Euros he received in Kristo’s Estonian bank account. And Kristo would reciprocate by depositing pounds in Taavet’s bank account.

With this, neither had to pay an extra penny in hidden bank charges.

This eventually saved them thousands of euros and pounds. The problem, they saw, was obvious. The system for cross-currency transfers was broken. And the private peer-to-peer money transfer system they had come up with was a proof of concept for how it could be solved.

Almost in frustration then, Taavet and Kristo founded TransferWise in March 2010. Soon, they got licenses from UK Financial Services Authority and HMRC to operate as a foreign exchange and money remittance organisation. And finally, in January 2011, they launched the peer-to-peer currency exchange that would compete directly against the banks.

Taavet’s seven years at Skype made him bullish that TransferWise could “do to currency exchange what Skype did to telecommunications”. Their experience earlier had also set the vision for the company, which revolved around providing a fair financial service. I will get into the weeds in a while. But before, it is important to understand the depth of the problem with international money transfers that continues to this date.

How do traditional banks do international money transfers (remittances)?

This is best understood with an example.

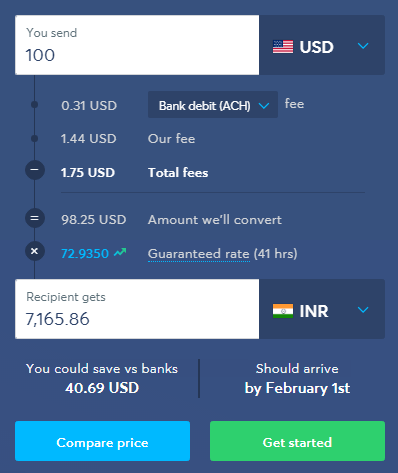

Imagine that you are sending $100 from your bank in the USA to your bank in India.

You would likely log on to the wire/ACH transfer page of your bank in the USA,

Select the currency (INR) you want to convert the money into, and

The bank will quote you an exchange rate and the transfer fees

Say that the exchange rate it quotes is 70 (=USDINR), while the transfer fee for providing this service is $0 (for simplicity). In effect, your outgoing $100 would become INR 7,000 on arrival (say, within 1-3 working days).

For an average joe, who understands little of the banking world, the “best offer”, “free money transfers” or “0% commission” claim made by the bank would seem true seeing the 0% transfer fee. But for you, who knows how foreign exchange rates work, the happiness would be little. You realise that the mid-market rate, i.e. the real-exchange rate – around the average of the bid/ask rate for a currency pair, for USDINR is quoted at ~72 on Reuters. Your bank, like every other, had set its own exchange rate of 70 for the day. And made INR 2 for every dollar you converted.

Your $100, in an ideal world, should deposit ~INR 7,200 in your Indian bank account. But the hidden mark-up on the exchange rate meant that only INR 7,000 was deposited.

The question then arises: why are you not able to transfer at the mid-market rate?

Two reasons. First, providing this service costs bank some money and they want to recoup that. Second, banks see this as an opportunity to make profits since the public is 1) largely not aware of the hidden fees, and 2) don’t have many choices. The latter is usually the bigger reason, but don’t say it out loud.

Now, remember that banks do charge some transfer fees, unlike as stated in our simple model. But, they also continue to derive most of their revenues through the hidden charges in exchange rates. In fact, a leaked memo of Bank Santander a few years back revealed that the bank made €585m in revenues through remittances in 2016. And ~50% (€290 Mn) of this revenue was through foreign exchange mark-ups and the rest was divided between fees and correspondent banking services.

The costs for remittances, even today, remain high. We see that the buy and sell currency rates are marked-up 2-4% to either side of mid-exchange rates (above), with the transfer fees as additional costs. The spread only gets higher as we go to currency pairs with less liquidity.

Taavet and Kristo set out to solve exactly this fair exchange rate problem with TransferWise.

Personal experiences made them realise that customers wanted cheaper and fairer remittances. And the effectiveness of their private agreement system gave way to build TransferWise.

So, how does TransferWise work?

True to their goal, the platform offered – and still does - conversion at the exchange rate equivalent to the mid-market rate, i.e. there is no intended mark-up on conversion. They can do that since the mid-market rate is surprisingly easy to fetch. TransferWise uses the rates available on Reuters, but you can likely use Google, XE, Bloomberg, and get similar quotes.

But how do they cover their costs then?

Two ways: 1) TransferWise charges a transfer fee, which might be higher than that offered by banks and money transfer operators, and 2) follows a peer-to-peer model. The second point probably raises more eyebrows. Let us understand it better.

In a traditional banking model, the sender’s bank would use SWIFT to send out a payment order to the receiver’s bank. Once the confirmation of the message is received, the correspondent accounts that both institutions have with each other would settle the actual transfer. In this system, the money has to cross the bank account in one country to the corresponding account in another. There have been few innovations along the way, but this process remains costly, time-consuming, and opaque.

Instead, in the peer-to-peer transfer model of TransferWise, money never really crosses borders.

TransferWise does that by holding bank accounts in countries it allows the transfer of money from or towards, matching the transactions of users across its platform, and settling the money in the local TransferWise accounts.

To use a simple analogy, if X wants to send US$100 to India and Y wants to send INR7,200 to the USA, then the amounts are hypothetically matched (assuming mid-market rate at 72). In this case, X’s bank transfers money to TransferWise’s local bank account in the USA, while TransferWise’s local bank account in India transfer’s INR 7,200 to the bank account that X was sending the amount to. The local bank accounts of TransferWise play the opposite role in the case of Y’s transfer.

Regardless, the money is settled with the local TransferWise bank accounts and not directly between the sender and the receiver. This means that the money, theoretically, never crosses borders. And peer-to-peer matching implies that TransferWise does not have to hold all the money they have to send.

Of course, for every X, there is likely not going to be a Y. That is, peer-to-peer matching would not take place sometimes. In such a scenario, TransferWise must act as a market maker by keeping the deposits in local currency liquid. This comes with costs and the cost is internalised in how transfer fees are calculated basis geographies and amounts of transfers.

Overall still, the process saves TransferWise ~5-10X of the transfer costs of a traditional bank.

People aware of the hidden costs were quick to latch onto the platform, with TransferWise processing transfers worth €10 Mn in the first year of operations. The number of transactions was only ~5,500, but the platform saved customers €500,000 in fees. This was considerable and proof that their model worked.

Investors followed, with Paypal co-founder – Max Levchin – investing in 2012, and several incl. Peter Thiel and Richard Branson soon afterward.

By mid-2017, the company was processing transfers worth over €1Bn monthly and had turned profitable. Fast forward to today, and the company claims to send $6Bn every month, saving over 10Mn customers a handy $1.5Bn every year.

Although their core model has remained the same, product innovations and a strict focus on the company’s values have allowed them to grow faster than people anticipated. Let me elaborate.

TransferWise has refined its principles from the earlier “No Bank Fees” to one where moving money abroad is cheaper, faster, and fairer in more ways than one. We get the picture when we go through each of their values.

Be radically transparent

Transparency is at the core of offering fair remittances, and produced by keeping none of the costs hidden. The transfer fee and mid-market rates for 70+ currencies are calculated and presented live on the exchange platform.

But the keyword in the value is radically.

Not only are the fee and exchange rates transparent, but the platform is also honest in comparing its charges across banks and other exchange platforms. For example, if there is a cheaper alternative for a particular remittance transaction – the comparison tool on the platform shows that TransferWise is not the cheapest.

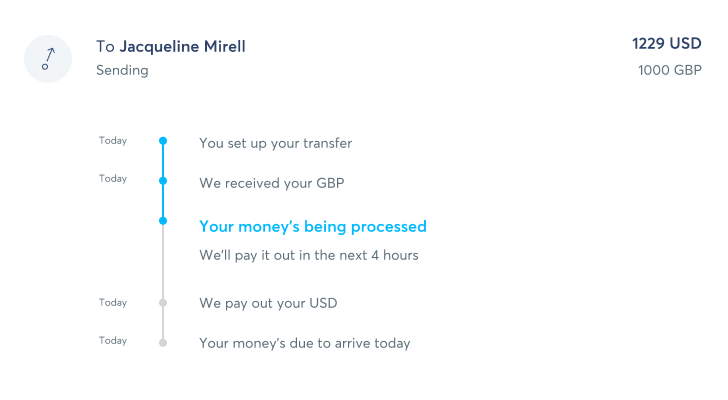

Next, once a transfer is initiated, the platform allows customers to track the transfer as an Amazon would do for a smartphone you had ordered.

Combined, these features help establish trust in the company’s mission to be radically transparent and differentiates it from the regular banks and money transfer operators.

Charge as little as possible

TransferWise explicitly states that the pricing of their transfer fee is not to maximize profits but to maximize the savings of the customers. That is, it charges what it costs the platform to send the money plus a small margin that makes existence feasible for the company. The claim is validated by how the average costs on the platform came down initially as the company scaled to a higher number of customers.

Saying that, the average transfer fee also increases in times when the operational costs go up. We see, in the graph below for example, that the fees went up during Q3 2019 as some of the routes became costlier. But the candidness and transparency of the founders allow customers to trust the rationale behind the increases, which is a testament to their clear mission values and communication.

The pricing structure has also evolved to the benefit of customers. Initially, the platform would charge the higher of the flat fixed fee (say, €1) or a fixed percentage of the transfer amount (say, 0.5%), both adjusted based on the currency pair. But then, in 2018, the fee structure was revamped to a fixed + variable component. For example, a 0.35% + £0.60 when sending from GBP to EUR. The fixed and variable fees are adjusted basis the currency pair, mode of transfer, route costs, and on and on. For any given amount, you can check the fixed and variable costs easily on their website.

Finally, staying true to the ‘as little as possible’ mantra, the company periodically publishes the breakdown of their average fee into costs and margin over and above.

We see here that the surplus margin around Aug ‘19 was ~18% of the transfer fee. This would imply that the company was making a profit of only 0.12% (Average fee = 0.70%) for every unit of the amount they moved. Not a figure you can hold against them!

Make premium the new normal

The mission here is to ensure that each TransferWise user is offered the best possible service. The best service for TransferWise suggests providing the fastest possible route, the lowest fees, customer support in preferred languages and timezone, and no tiered pricing or subscription services based on subjective criteria for transfers.

We see that ~81% of all transfers on the platform today are completed in <24 hours, up from ~55% in early-2018. The share of real-time and <1 hr transactions have also gone up significantly. The latest mission update highlights the direct integration with the central bank in Hungary and better pay-in speeds in the USA and Canada as the major forces behind the improvement.

Besides, the peer-to-peer model, improved liquidity management, and new operational partnerships are equal reasons behind the high speed of these transfers.

To improve the experience further, the company has continuously improved the accuracy of the transfer forecasts over the last three years.

The share of transfers that reached later than estimated delivery time, for example, has fallen from ~30% to 11% in the three years. A significant improvement.

TransferWise leverages the general public distrust in banks by being superior on all three mission values, and also continuously adds new products to its offerings to challenge the cross-border banking revenues.

Remember the leaked Bank Santander memo that was mentioned earlier? If the bank had charged customers what TransferWise did in 2016, their revenues would have been only €95Mn, instead of €585Mn – a drop of 84%!

Multi-Currency Account and Debit Card

In 2017, TransferWise launched a ‘Borderless’ account (now called multi-currency account), targeting businesses, sole-traders, and freelancers. The online banking account was meant to target the groups that transact in multiple currencies, and today, the account has the following features:

Convert and hold your money in up to 55 different currencies in the account

Receive and make payments without added fees (like a local) in up to 9 currencies

Send money, as you would using TransferWise, at rates up to 8X cheaper, and

Use a debit card to spend in 200 currencies, converting the money using mid-market rates, with the added functionality of using Apple Pay and Google Pay

Some of the features are restricted in certain geographies and this page gives a clear view of what features you can avail in your country. The core purpose of the account remains to allow users to hold and transact in multiple currencies at a fair exchange rate.

TransferWise continues to add new features and geographies to its multi-currency account. In Q4 2020 update, for example, the company highlighted the availability of debit cards for users in Japan and recurring transactions using the account as new additions, among others.

TransferWise for (Neo) Banks and Fintech Businesses

The company also provides easy API integrations to banks with limited currency exchange capabilities. This improves the value proposition of the banks, offers TransferWise an existing user base, and reduces the effort all around. A win-win for everyone. Presently, TransferWise powers remittances for N26, Monzo, bunq, Novo, Pockit, among other popular neo-banks. And today, 9 out of every 10 bunq customers use TransferWise to send money abroad.

Additionally, TransferWise offers this integration for free to the companies, earning only from the transfers from customers on the platform. Emburse, an expense management system, is one of the latest additions to the list of fintech businesses integrating the service.

The integration is a great growth lever for TransferWise, and we can expect it to push harder towards API integrations to expand its ecosystem.

TransferWise for Businesses

While the integration is quite plain vanilla for banks, it is much more sophisticated for businesses. With the international business account on TransferWise, businesses small and large get to:

Pay invoices, handle inventory and payroll, and exchange money in 50+ currencies – 19X cheaper in some cases

Transfer to accounts without the recipient holding a TransferWise bank account

Avail spending benefits of TransferWise at mid-market rates with Business Mastercard cards

Process batch payments and assign roles within the company to handle transactions and accounts

Connect with account management tools such as Xero, Quickbooks, etc.

The team continues to add functionalities for the business customers, incl. multiple debit cards and faster onboarding – as they shared in the latest update.

The Road Ahead

The singular focus on money without borders has meant that all operational improvements and product innovations combine to lift customer experience on TransferWise. As the company has scaled, the efforts have translated into a strong balance sheet with:

Revenues for FY 19/20 at £302.6 million, up 70% YoY from £179 million in FY 18/19

Three consecutive years of profitability, with £21.3 in net profit after tax for FY 19/20

Over 10,000 new users joining every month, with the APAC region as the fastest growing

Going ahead, the expectations for revenue and profits remain as optimistic for TransferWise. The last round of capital raise valued the company at $5Bn, with the valuation expected to be closer to $10Bn today. For those interested, below are the four developments that, I believe, should gather growth momentum for TransferWise:

IPO: TransferWise has selected Morgan Stanley and Goldman Sachs for its London exchange listing, which is expected to take place in 2021. Given the growth and the healthy financials, expect it to be a much-revered listing.

Partnerships and more Partnerships: the company has expanded a lot of its energy into the geographical expansion of multi-currency accounts and debit cards – both of which bring higher lifetime value from customers by making them more loyal. The latest partnership with Visa would allow it to speed up the process by accessing VisaNet on the cloud. This does away with the significant investments that TransferWise would have had to make in local infrastructure in new geographies. Expect TransferWise to double on API integrations and partnerships with fintech companies to further speed up the adoption of its multi-currency accounts and debit cards.

More focus on businesses: With features such as multiple debit cards and the wind moving towards more remote and borderless businesses – TransferWise for Business segment is where the company will further differentiate itself from banks and MTOs. The value-added features of processing payrolls, invoicing, multiple user controls are especially useful given the pressure that TransferWise faces now from banks such as HSBC following the company’s steps.

Faster payments: with the central banks around the world moving towards real-time payment rails, a big test of TransferWise’s capabilities will be how it manages the liquidity to process more transactions instantly. Experience with instant payments in countries such as UK, Hungary, should allow TransferWise to integrate the rails faster than the incumbent banks.

Today, the company has 14 offices across the world and over 2,200 employees working remotely. With the IPO, Visa partnership, and new competition from banks – 2021 will be a year to watch out for TransferWise. I, for one, am betting on TransferWise to come out flying on top!

Other interesting reads on the topic:

On how TransferWise is building a Global Financial Services Brand by Igor Gorbatko

On Q4 2020 Mission Update by Kristo Käärmann at Transferwise

On developments in the International Money Transfer market (2016) by Mauro F. Ramaldini

If you have any views or feedback to share, feel free to add a response below or to share your thoughts with me over Linkedin. In case you feel your friends or family would be interested in reading about fintech or economics, feel free to share the blog with them as well. See you in a week or two!