Spotlight on QR Codes (#25)

Also: how QR stands out, discussion around interoperability, and other challenges

Quick-Response (QR) codes are not new. They were first patented and used in 1994 in Japan. The purpose then was to track vehicles at high-speed while manufacturing. Twenty-seven years later, the usage is significantly wider. Tracking aside, QR codes are used simultaneously for consumer-convenience purposes. These include ordering at restaurants, scanning for information at retail stores, connecting to Wi-fi, and payments at the point-of-sale. The focus of this article is, expectedly, on payments using QR codes and on how such payments are seeing a resurgence in the developed world. I will also briefly touch upon the technology behind the codes and on why interoperability is a big talking point in QR today. Let us begin.

The QR Craze Travels West

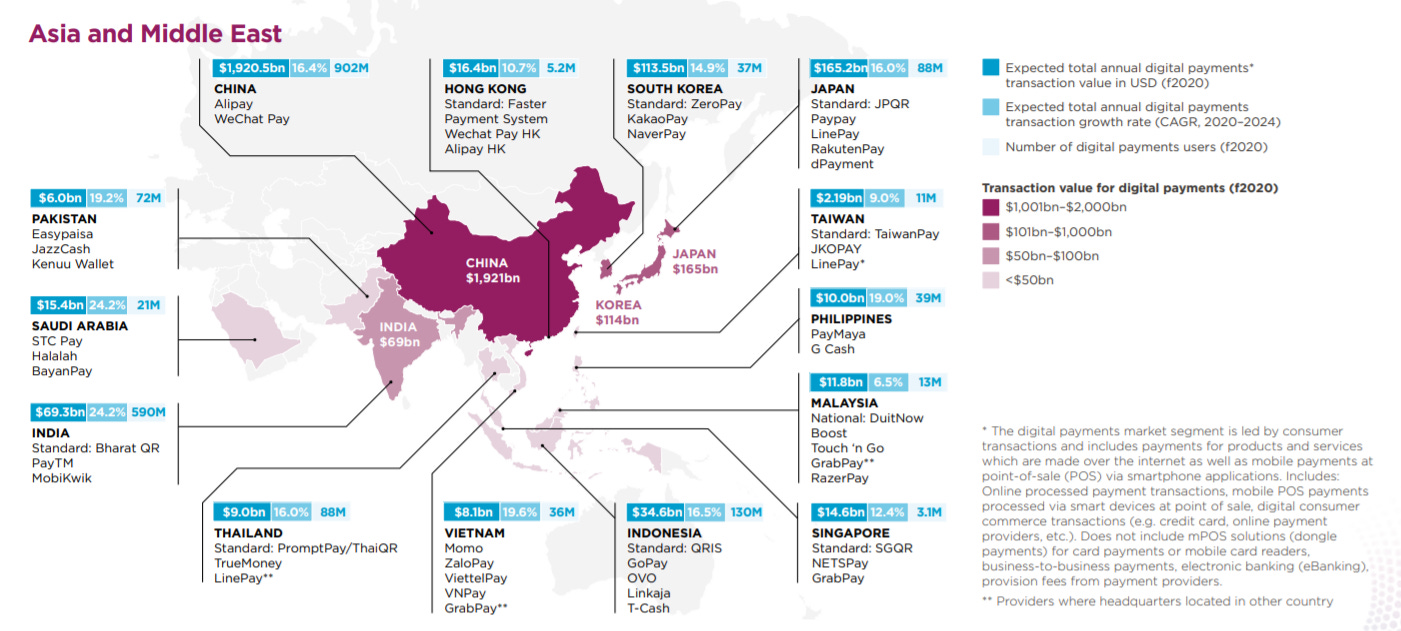

China has been the greatest exponent of QR payments for the last decade. With the Alipay and WeChat wallets, and a broken credit card system, the country has largely depended on mobile payments. So much so that over 90% of customers see the two wallets as their primary means of payment today. Both the wallets use QR codes as their preferred mode of transactions, with the payer and the payee both able to provide their unique bar codes for scanning.

The latest survey by UnionPay paints an even more dominant picture. In 2020, ~98% of the Chinese customers pointed to mobile payments as their most commonly used mode of payment, with 85% of the respondents using QR to pay in 2020. Such is the frenzy that you are likely to even see beggars carry QR codes instead of tin bowls for collecting donations in China.

The other countries have been a little slower to adapt to QR payments. But with the smartphone penetration increasing, internet connectivity getting faster, and mobile wallets becoming a common method of payment at POS, many in Asia-Pacific have developed affirmation for the QR method. India, in particular, is a successful case study with Paytm leading the push through its all-on-one QR system, followed closely now by the likes of PhonePe, Mobikwik, Google Pay, and BharatPe. The narrative for QR is furthered in India by the almost negligible data costs, some radical government measures, and the support of RBI and NPCI with Bharat QR and UPI QR initiatives.

Something similar has transpired in countries close-by, namely in Japan (PayPay), Indonesia (Go-Pay), Singapore (GrabPay), South Korea (Tesco), and Hong Kong (PayMe), with the QR usage becoming widespread. The shift towards QR has been continuous in APAC, but the same fervour is not found in countries towards the west.

In the USA, the risk of fraud through virus-infected QR codes, the lack of knowledge, and the consequent misuse of QR codes combined to create a trust deficit in the country for the method. The same was true of Europe, where QR payments fell behind the card and NFC-based mobile payments despite the presence of large wallet providers.

For example, Apple Pay, a leading payment method in the USA, had opted for NFC (near-field communication) technology for in-store payments, which has remained the dominant method over mobile for the last six years. It had intentionally left out QR codes as their use had gradually waded in the country. This was equally true of Samsung Pay. They had instead opted for a physical debit / credit card along with NFC wallet payments, instead of QR at the point-of-sale.

But with COVID-19, QR codes have assumed a new meaning. The need for touchless ubiquitous commerce along with the ready standardization of QR codes at scale have made the transition for people quite convenient. This is visible in how payments companies and businesses are flogging towards adopting it.

PayPal introduced QR codes in May 2020 and has since expanded PayPal and Venmo QR to over 600,000 retailers, including to the likes of Nike and CVS. Moreover, such merchants have seen basket sizes grow at double-digit rates among consumers who frequently use QR codes, highlighting the effectiveness of QR codes.

In other news:

Square, a major POS-systems provider, introduced QR-driven Square for Restaurants platform, allowing customers to scan menus, order, and pay by scanning QR codes.

Apple is mostly adding QR-functionality to Apple Pay, after long consideration

Mobile-ordering platform LevelUp partnered with Toast POS to allow touchless bill payments at restaurants

Walmart added QR codes to Walmart Pay to allow millions to shop contactless at its stores

A study by Mobileiron recently found the trend gain speed in the UK and European Union as well. The survey, conducted in September 2020, saw ~80% of smartphone users mention that they had used QR codes at least once in their lifetimes and 40% said that they had used QR in the past week. Interestingly, more than half the respondents said that they expect to use QR codes in the near future as well.

The idea here was to highlight the tremendous push that QR payments have got in the more developed parts of the world. The question, however, that arises is whether we expect this trend to stick. That is, is it only a temporary change forced by the pandemic or is the change in behaviour and the western attitude fundamental?

The short answer is that the adoption of QR code payments is largely fundamental and long-term, particularly due to the design standardisation, mobile and internet pervasion, and regulatory & business push. I will elaborate on these points and the why in detail, but before, let’s understand how QR works.

What are QR Payments?

QR codes are 2-D barcodes that are capable of

Storing a large volume of data

Being scanned from one screen to another, without the need for paper

Being read despite some damage to the code

Compared to the 1-D barcodes we see on food items inside stores, QR codes are read 360 degrees, i.e. both horizontally and vertically by the scanning software. QR codes come with varying degrees of input mode, character storage limits, and encoding standards.

But without going into the details of the technology (not that I know much of it), it is important to note that at the point of sale, there at usually three methods of scanning:

Dynamic QR Code (Merchant): merchant integrates dynamic QR codes into its payment system, and displays them on a screen to the customer. The customer then scans the merchant’s QR code to pay.

Static QR Code (Merchant): no technology or equipment is required in this case, with the merchant showing a static QR code associated with it acquired from a bank or a payment service provider. Similarly here, the customer scans the code that may be printed on paper to make the payment. This is rather common in Indian shops.

Consumer-presented QR Code: here, once the merchant confirms the transaction details, the consumer presents the QR code and the merchant then completes the transaction by scanning it. This is done by providing a unique QR code to each customer account within the QR payment application.

This was mostly common knowledge, but what remains a puzzle at times is the utility behind the method.

So, what makes QR Codes stand out?

The convenience of simply scanning a QR code was always there. But other factors have made QR prevalent today:

Alternative to expensive POS: a typical POS machine costs around ~INR 5,000-12,000 in India, and with millions of small shops hard-pressed on money (especially during the pandemic), QR codes presented a cheaper and equally effective alternative through static codes.

Fast internet connectivity: internet ubiquity in many parts of Asia and, less so, in Africa have lowered the failure rate of QR scans, and the high data speeds have made the transaction times lower

Bank Account & Smartphone Distribution: penetration of banking and smartphones in, especially, the developing world has made the device and formal identity affordability significantly higher. Moreover, since 2017, Android and iOS smartphones have introduced standards that make them compatible to read QR codes, which has made the usage of QR codes a lot less puzzling.

Wallet Penetration: The smartphone distribution has complemented the development and spread of local wallet systems, which act as the ideal providers of QR code payments.

More than Payments: compared to other payment methods, merchants are incentivised to use QRs as they can offer more services – read menus, link to shop website, referrals, social media pages, sell complementary goods – with QR codes. This would have likely tilted the balance towards QRs for many restaurants and other smaller merchants that wanted to increase visibility during the pandemic.

It is important to understand that among all the POS payment form factors – debit / credit cards, mobile wallets (non-QR), cash – none is as inexpensive and accessible, while being equally convenient, as QR codes.

The method lowers the acquiring cost of merchants, while providing customers the convenience of not needing to input any merchant-specific data. The potential of using QR for all sorts of payments – utility, grocery, fuel, food, travel – without any supervision also makes it popular within crowds once the initial hesitancy is overcome.

These points are true for customers and merchants in both developed and developing regions. However, the degree and drivers of adoption continue to vary between markets.

In Africa, deficiency in smartphone and internet infrastructure has meant that QR codes remain an experiment for private mobile payment providers. Challenges remain also due to high levels of the underbanked population.

In developing countries such as Indonesia, Thailand, the QR push is regulator-led with the focus on financial inclusion and providing means of low-cost, non-cash merchant payments. Government benefits by pushing QR due to higher money traceability and potentially higher tax revenues. India, with similar motivations, is seeing a combination of large private sector players and regulators to make QR codes a commodity through interoperable QR codes, i.e. QR codes that can be scanned by different mobile payments applications.

In more mature markets such as Taiwan, EU, UK regulators have taken it upon themselves to ensure domestic interoperability, and in some cases, cross-border interoperability of QRs.

Others, such as the USA, see QR push mainly dominated by deep-pocketed companies such as Square, PayPal, and Walmart.

These trends establish the government / regulator-led approach towards QR payments as particularly important. This is largely down to making the method cheaper by standardizing the divergent specifications that have developed as part of the QR ecosystem.

Interoperability and What’s Ahead

Many markets around the world are currently nearing the maturity phase of QR system development. With mass adoption, the focus is now moving towards making the systems more commoditised by moving from a proprietary, closed-loop scheme to one where the QR codes are domestically interoperable.

This is evident with private players, governments, and central banks in India (Bharat QR, UPI QR), Singapore (SGQR), Japan (JPQR), EU, among others adopting measures to harmonise specifications for QR code payments. The implication on the scale and growth of the systems is significant in later stages of ecosystem development.

For example, interoperable QR codes offer higher convenience to merchants, who don’t have to maintain multiple QR codes, and to customers, who can transact at all QRs with just one favourable application. This also shifts the competition away from the distribution or from acquiring merchants towards simply offering better services or attracting customers.

The approach towards interoperability is hardly linear, however. The report by GSMA details in great depth the two integration approaches, harmonised QR or back-end API, for interoperability. It also expands on the type of agreement structures, geographic considerations, and directionality of interactions that are considered during the process. I would strongly recommend going through it for a better understanding of this particular situation.

Lastly, despite all that is going for QR codes, there remain challenges to the growth of the ecosystem, particularly the following:

Regions with developed internet and banking infrastructure, such as in Europe, see QR as comparatively inconvenient and are expected to remain card dominant

Biometric payments are touted as the next contactless and truly secure method of payments. With the costs of POS terminals gradually falling as mPOS becomes standard, NFC in cards going mainstream, biometric payments are likely to become low-cost, contactless, and offer higher security than QR codes.

Talking about security, the diverse nature of QR codes and the lack of information on what stands behind one – especially on the internet – make fraud a definite possibility. Overcoming this would likely introduce friction in the payments process or high costs in making people aware, both of which are deterrents to QR usage. In fact, the survey by Mobileiron showed that 44% of respondents across the UK and EU have security concerns with QR.

These factors, along with the low level of QR standardization across borders and insufficient mobile and internet infrastructure in certain regions remain interesting challenges for the future of QR code payments. With competition for the low-margin and scale-dependent QR payment method, expect a high level of consolidation amongst providers as markets become more mature. But till the pandemic exists, QR will remain the king!

Other interesting reads on the topic:

On QR growth opportunity for Mobile Money Providers (Report) by GSMA

On the state of QR in 2020 by Blue Bite

On QR Codes - The New Age Tech Shaping India’s Digital Payments Landscape by Vishal Anand for NPCI

If you have any views or feedback to share, feel free to add a response below or to share your thoughts with me over Linkedin. In case you feel your friends or family would be interested in reading about fintech or economics, feel free to share the blog with them as well. See you in a week or two!

Very good article! Super interesting to see its cost benefits compared to other options like POS. It's truly boosted through the pandemic versus NFC, for example