Talking Points on Charges in Indian Payments (#56)

RBI questions the existing payment charges, and seeks feedback on what and how it should regulate

Welcome to the 56th issue of Unit Economics. For today’s write up, I review and share my thoughts on the “Discussion Paper on Charges in Payment Systems” published by the RBI. Dive in!

On 17-Aug, the Reserve Bank of India (RBI) published a discussion paper on charges in Indian payment systems since it “considered necessary to undertake a comprehensive review of the rules and procedures for levying charges… assessing their impact on the efficiency, growth, and acceptance of payment systems”

With this objective, the paper details the existing rules and manner of charges applied to the many payment systems, argues for and against alternate payment rules within each, and presents a set of questions to seek public feedback on. The document suggests that “based on the feedback received, RBI would endeavour to structure its policies and streamline the framework of charges for different payment services / activities in the country”.

The unbiased posing of arguments and the invitation for dialogue shows a welcoming and proactive approach to the discussion around payment charges. I will attempt to review the paper from a similar perspective.

The Two Types of Payment Systems

The paper defines a payment system’s function as one to settle financial transactions, wherein the flow of funds may involve (A) a movement of funds from one account to another, (B) loading of cash to an account, or (C) withdrawal of cash from an account.

To add structure to the discussion, the payment systems are categorised into two branches: (1) Funds Transfer Payment Systems, and (2) Merchant Payment Systems.

How are they different?

The Funds Transfer Payment Systems are systems that facilitate transfer between two accounts with the recipient account identified by the originator customer. Such systems are also popularly referred to as person-to-person (P2P) payment systems, although the purpose of transfer may remain for the purchase or sale of a good or service.

Further, for transactions in such systems – the charges are “generally recovered from originator of the payment instruction… levied as an add-on to the amount earmarked for remittance.” Moreover, the charge is often uniform or fixed, i.e., levied on a per transaction basis irrespective of the transaction value.

Merchant payment systems, on the other hand, are used for availing goods or services, enabling what we refer to as person-to-merchant (P2M) transactions. In such systems, the charges are instead recovered “by deducting the same from the amount receivable by the merchant, i.e., a discount to the amount receivable by the merchant” known as Merchant Discount Rate (MDR), which is then divided and distributed with the issuer and other intermediaries via interchange, switch fees, and other charges.

Herein, the merchant may choose to pass the costs to customers in the guise of a surcharge or convenience fee – however, the practice is discouraged and sometimes forbidden. Further, the MDR and other charges are relatively less uniform in nature and may differ based on the channel, medium, and location of the transaction and/or on the size or relationship of the merchant, which is unlike the charges in fund transfer payment systems.

Product-wise Discussion on Payment Charges

The paper goes on to categorise each payment product under the two payment system categories.

Under Funds Transfer Payment Systems, the paper covers the Real Time Gross Settlement (RTGS), National Electronic Funds Transfer (NEFT), and Immediate Payment Service (IMPS) systems.

As for the merchant payment systems, it covers Card Networks - including Debit, Credit Cards - and Prepaid Payment Instruments (PPIs). UPI, it suggests, overlaps both categories of payment systems by providing the utility of real-time transfers for P2P, and the ability to handle low-value transfers with convenience for P2M.

Given this context, I will share the key features on payment charges for each payment system, and confront relevant questions where possible.

Real-Time Gross Settlement (RTGS)

The RTGS system regulations impose a monthly membership fee on direct members

RBI discontinued levying processing charges and time varying charges, on members from July 1, 2019

RBI has prescribed that no charge can be levied by members to the customers for inward transactions

The maximum charges permitted to be levied by members for outward transactions have been defined by the RBI

Banks are free to follow their internal policy regarding their customers subject to the overall cap. For example, Some banks do not levy any charges for RTGS transactions initiated online

On RTGS, the RBI questions whether it would be justified to recover the cost of its large investment and operational expenditure in enabling the payment system from the members.

View: given that these costs from RBI involve an expenditure of public money, the regulator bears an almost moral responsibility to recoup it back. However, given that the RBI would act as a not-for-profit, it would make sense for the regulator to adopt a policy of charging a direct fixed price to members, such that the overall earnings from the fixed charges allow it to earn what economists call normal profit, i.e. wherein revenues equal the sum of implicit and explicit costs borne. These charges can be reviewed semi- or annually to ensure accurate fixed pricing.

National Electronic Funds Transfer (NEFT)

RBI does not levy any processing charges on member banks and has also advised banks to not levy any charges on savings bank account holders for fund transfers initiated online through NEFT

RBI has prescribed the maximum customer charges (exclusive of taxes, if any) for outward transactions undertaken using NEFT initiated through branches.

Similar questions arise for NEFT transfers: should the RBI charge member banks for transactions processed through NEFT given the infrastructural costs? Should banks be permitted to charge customers for NEFT transactions? If yes, should RBI prescribe these charges?

View: similar views, as for RTGS, follow for RBI’s stance on charging member banks, with the suggestion for a fixed pricing model priced to drive normal profits for the regulator. On the second question, it follows that if the RBI must charge members to recoup their costs – treatment of the payment system as a public good where customers are not charged would be inappropriate.

More importantly, curbing all charges would be harmful to member banks who incur man-hours, and other maintenance and operational costs to process NEFT payments. And on the question of whether RBI should prescribe such charges to member banks, the degree of regulation presently practiced via price ceilings appears sufficient to save customers from exploitation – and it would perhaps help member banks if, how it does for Debit Cards, the RBI can adopt a differentiated fixed price ceiling model. This would allow the more deficient member banks to charge relatively higher for the provision of NEFT services since the proportion of costs incurred on the upkeep of NEFT systems out of their overall costs is expected to be higher.

Immediate Payment Service (IMPS)

IMPS is operated by NPCI and settlement in IMPS is on a deferred net basis

Charges are imposed on the originator in an IMPS transaction by the participating bank. NPCI in turn imposes transaction fee on the participant banks to recover its cost of operations

While UPI transactions are mobile based for the customers, IMPS transactions can be initiated using other devices also. Besides banks, IMPS allows non-bank entities such as PPI issuers to participate and facilitate remittances from wallets

Given the pace of growth in IMPS transactions despite the availability of other systems, the RBI wonders (A) whether it should regulate IMPS, and (B) whether it should fix a ceiling on charges that can be imposed on IMPS.

View: On the question of whether RBI should jump in to regulate IMPS – it appears that given the pedigree of the payment system in line with that of NEFT and RTGS, the involvement of RBI would lead to more uniformity across fund transfer payment systems. Only last year, the RBI raised the transaction limit from INR 2 lakh to INR 5 lakh, promoting the use of IMPS for larger ticket sizes.

Further, quick research on NEFT and IMPS rates across member banks shows that IMPS rates are ~1.5 to 2X of the caps mandated on NEFT for low-ticket size transactions upto INR 1 lakh, which – if the price ceilings on NEFT are to be taken as sacrosanct – should call for similar intervention on IMPS. However, the decision on price ceilings will depend on the cost of operations of the particular payment method, which may vary from that for RTGS or NEFT.

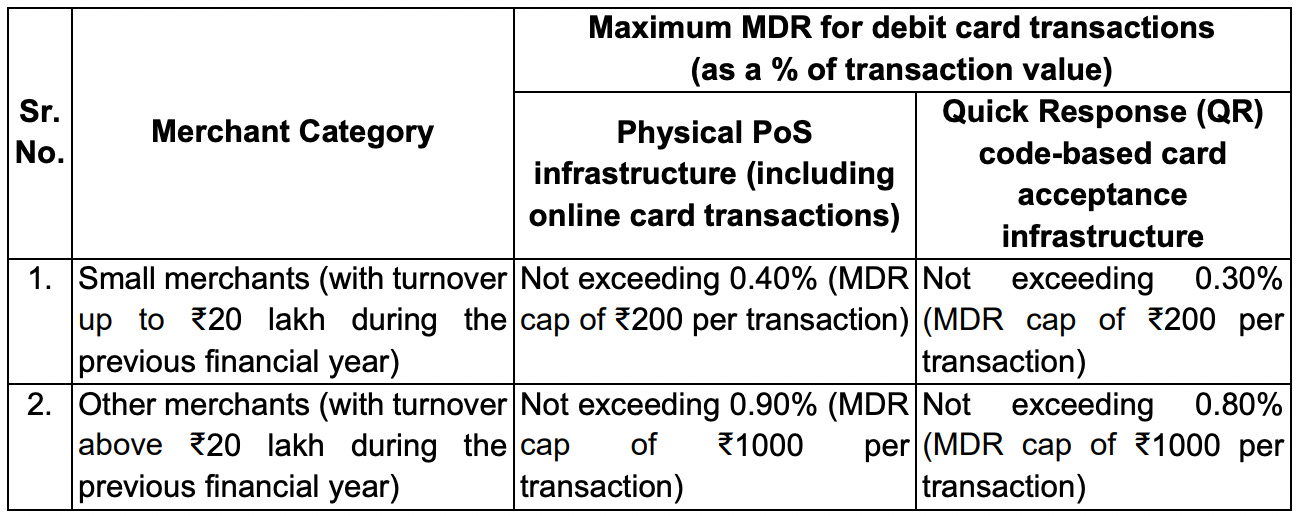

Debit Cards

Only merchant payment instrument where RBI has intervened to bring down the cost to merchant

With effect from Jan-18, RBI prescribed the below charges as maximum MDR for debit card transactions

The cost to small merchants for accepting debit card transactions has come down substantially since the mandate

Government, vide amendment to the PSS Act, has made the MDR for RuPay debit cards (and UPI) zero, effective January 1, 2020

In order to balance the costs to merchants and returns to payment system operators, the RBI discusses multiple alternatives to managing debit card charges. It suggests that to give acquirers higher flexibility on MDRs, the interchange – which forms a part of MDR - can be regulated.

Given the strict caps on MDR for debit card transactions, the lack of interchange regulations has likely squeezed margins for acquirers. This is particular to card transaction economics given the incentives in the 4-party model encourage card schemes to offer higher interchange fees to issuing banks for winning partnerships. With this context, it would appear almost natural for PSOs – especially acquirers - to demand similar regulation of interchange on card networks.

While contemplating interchange regulation, the RBI then wonders whether the charges on debit cards should be as a percentage of the transaction value (ad valorem) or a fixed amount irrespective of the transaction value. In this regard, it surprisingly takes a position for the latter by arguing that “as cost to issuer / acquirer does not generally depend on transaction value of a debit card transaction, the charges could be uniform for all debit card transactions, irrespective of transaction amount”.

However, it would be unlikely if the costs were to be similar across transaction values, given that the costs of fraud risk management and rewards are often linked directly to the transaction value. If the cost is positively correlated with the transaction amount, it will make sense for the regulator to consider an ad valorem cost structure for lower amounts. To ensure that the ad valorem costs do not make high-value transactions disproportionately expensive, a fixed cost structure may be applied above a certain ceiling of the transaction amount.

Lastly, zero-MDR on the RuPay card network has helped tremendously to increase merchant acceptance for the network. But with the costs of deploying infrastructure for acceptance at PoS or of processing payments – the acquirers and issuers should no doubt earn similarly on RuPay as they do for other international card networks. If NPCI or RBI so wishes to treat RuPay as a public good, a quarterly or half-yearly reimbursement to PSOs and intermediaries should be formalised and made a norm.

Credit Cards

The main differentiator in a credit card transaction is the credit component and the risk of default arising therefrom

RBI has not issued any regulatory mandate or intervened on MDR for credit card transactions. The main reason for this is the credit linked nature of the product.

While many a time, the increase in interest rates gets reflected in the form of a higher MDR, benefits of decrease in interest rates do not seem to be passed on to the merchants in the form of lower MDR

The RBI argues for a case to regulate MDR “as the charges for some credit cards are exorbitant and they do not come down with falling interest rates”. Given the relatively low total number of outstanding credit cards vis-à-vis debit cards, we may assume that the higher acceptance costs have hampered the adoption of credit cards in the country.

Following the same principle of balancing costs to merchants and the returns to service providers, the RBI has room to intervene similarly on credit card MDR and Interchange. Given the differing complexity of managing credit risk and fraud on different channels, a preference for tiered pricing caps on both MDR and Interchange would be natural.

Further, to ensure that the interchange revenue caps do not act as a barrier to entry or operation, differential pricing on interchange levels can be associated with the medium, small, and co-operative banks to encourage issuance – on the lines of the Durbin Amendment as applicable on debit cards in the United States.

Prepaid Payment Instruments (PPIs)

PPIs can be issued in the form of cards (prepaid cards) and wallets, and are akin to debit cards from the perspective of transaction processing

Non-banks operate PPI business as a standalone activity. They incur cost in operationalising the infrastructure for issuing and loading of PPIs as well as for providing merchant acceptance points. For a bank, the existing infrastructure like branch network, IT, etc., can be used.

For PPIs, there is a cost involved in loading the funds and this cost is generally borne by PPI issuer

Due to this cost of loading, the MDR for PPIs is kept more in sync with credit cards by the PSOs

RBI has not issued any instructions regarding charges for PPI-based merchant payments or funds transfer transactions

The market standard of syncing PPI MDR with that of credit cards appears too simplistic, and likely exaggerates the cost of loading funds versus the costs of managing credit risk. The present model calls for RBI to regulate MDR and Interchange similarly to that suggested for Debit and Credit cards.

However, for PPIs, the complexity of a tiered model may be larger given (A) the distinction in costs for banks and non-banks, (B) the varying sources of loading funds – bank account, debit card, UPI, etc., and (C) the form factor of a PPI – card versus a wallet. All of these factors should be considered in the tiered pricing model for the payment system.

United Payments Interface (UPI)

RBI has not issued instructions regarding charges for UPI transactions.

The Government has mandated a zero-charge framework for UPI transactions with effect from January 1, 2020 (paragraph 7.6). This means that charges in UPI are nil for users and merchants alike

Settlement among participant banks in UPI is on a deferred net basis. Facilitating this settlement requires the PSO and banks to put in place adequate systems and processes to address the settlement risk.

Merchant payments using UPI do not require installation of costly infrastructure by merchants as UPI QR codes are used

While the regulator asks whether a zero-charge framework is sustainable for UPI, it appears that the government is in no mood to allow a change. Given the costs of distribution borne by PSPs or TPAPs, of maintaining infrastructure for processing millions of daily transactions, and of onboarding and allowing acceptance of UPI on 30 Mn+ merchants – the zero-cost stance does have not a lot of ground to stand on.

But with the government’s view of treating UPI as a public good, the alternative for PSPs and intermediaries is to recoup the costs via government subsidies. However, until a methodology of distribution of government subsidies is formalised – it would be a fool’s game to depend on such costs.

If, however, the industry participants are able to justify a cost structure and convince the regulators – it follows that the charges on UPI should draw directly from those suggested on IMPS, given the overlap of the two systems. Further, the charges will need to account for the involvement of multiple additional parties - Third Party Application Providers (TPAPs), payer PSP, and payee PSPs – and the lower costs of merchant acceptance on UPI.

Lastly, given the low-ticket nature of UPI transactions – a direct fixed charge can be inordinately expensive for merchants, and it would instead make sense to follow an ad valorem MDR upto a certain transaction amount, post which a fixed charge may be applied to counter high percentage based MDR.

Final few thoughts…

In the discussion paper, the central bank interestingly suggests that “in any economic activity, including payment systems, there does not seem to be any justification for a free service, unless there is an element of public good and dedication of the infrastructure for the welfare of the nation”.

The treatment of payment systems as a public good is not unique to India. However, the grey line that allows the treatment of one method as a public good versus the other appears to be unclear to the RBI and the government themselves, let alone the payment system providers.

This was an underlying theme to the discussion on payment charges for all systems, where we noticed the RBI often wonder (A) whether it should regulate a payment system, and (B) whether the payment system should have costs associated with transactions. As a second-order effect, this produces ambiguity for the payment system providers that would have to think twice before entering a payment system.

An implication for the regulator here is to formally define and publish the distinction for payment systems as a public good, and to clearly identify the objective of their pricing decisions on different types of payment systems. This will help participation and make cost decisions for payment system operators and the intermediaries easier within each system.

As for the stance on payment charges - as with the digital lending guidelines, the RBI continues to put arms around those likely to be exploited (merchants) in discussion on payment charges.

With its unbiased approach to posing questions, the discussion paper does well to begin conversations around the payment charges – and as institutions, merchants, and the public share their views on the outstanding questions, the industry will keenly await a more sophisticated approach to pricing on Indian payments by the next year.

If you have any views or feedback to share on the topic, feel free to add a response below or to share your thoughts with me over Linkedin. In case you feel your friends or family would be interested in reading about payments, feel free to share the blog with them as well. See you in a couple of weeks!