The Digital Currency Experiments (#16)

Understanding the central bank digital currencies (CBDCs)

Last week, the Shenzhen government in China carried out a public lottery to give away 10Mn yuan (~$1.5Mn). This was remarkable for two reasons. One, you don’t see government lotteries every day. And two, the amount was issued in digital currency.

A government issue of digital currency has happened before, but this scale is uncommon. Over 2 million people applied, while only ~50,000 got lucky. The winners could simply download a digital wallet to redeem their 200 yuan (~$30) worth of digital tokens.

Interestingly, the internet information office in the state said that the trial was done to stimulate consumer spending. But this hides the true story.

This was not the first issue of digital currency by the Public’s Bank of China (PBoC). They ran similar experiments in April and across several cities – and with success. In the first five months since those issues, roughly ~3.13 million transactions worth over 1.1Bn yuan ($162Mn) had convened. Astonishingly, the digital currency had been adopted for over 6,700 use cases – from bills to government services.

Today, these trials are making small headlines. But their significance can’t be understated. Similar to the ingenious credit card trial by Joseph Williams in 1958 that gave birth to a trillion-dollar product, the government issued digital currencies can potentially change money forever. Possibly, to an even larger extent.

As pretty as the rationale for consumer spending stimulus may sound, the experiments from China hold a greater motive. For them, it all started in 2014.

Since the 1970s, China had gradually become strong. Strong enough by 2014 to consider challenging the United States as the most powerful and influential nation. The Belt and Road Initiative (BRI), and the previous attempts to internationalize RMB were steps towards this purpose. As ambitious as it may sound, China realised that acceptance of an alternate and superior payment system is what will break the back of the dollar. The discussions around decentralized cryptocurrencies were getting louder, and here, China quietly saw an opportunity and started acting.

In 2014, Xiaochuan Zhu – the then governor of the People’s Bank of China, established the Digital Currency Research Institute (DCRI), with the sole goal to explore the use of digital currencies by the central bank. In the same year, the Bank of England had published a research paper on digital currencies, rendering them incapable of posing “a material risk to monetary or financial stability in the United Kingdom” at the time. An indication that the central banks of the time were not considering digital currencies a serious threat to the monetary and financial systems. Call it inertia, lack of imagination, or some old heads at banking posts.

This was, however, not a deterrent to DCRI. Eventually, the institute ideated what we today know as the Digital Currency, Electronic Payment (DC/EP) – China’s potential answer to the dollar. If you think that these are similar to the Bitcoins of the world, there are elements of DC/EP that you must remember.

DC/EP is not a cryptocurrency

The primary goal of a cryptocurrency was to separate the state and the money. That’s why, for say Bitcoin or Ethereum, the value lay in their decentralized nature. DC/EP, much like other central bank digital currencies, is imagined on the idea of centralized control. It is state-backed and linked to fiat, and not free from them. In essence, DC/EP is RMB, only in digital form. It is not speculative and directly eats into the money in circulation (M0).

DC/EP is one coin, two addresses

DC/EP is not blockchain-based but only draws a few concepts from the technology. It is, but, One Coin. A coin guaranteed by PBoC and representing a specific value. The control is central. But, the structure is two-tiered. The two addresses refer to PBoC, which handles issuance, and commercial banks, and players such as Alipay, WeChat Pay, which will handle the currencies’ distribution. Moreover, the two sides will maintain their separate databases for the transactions.

DC/EP is not anonymous

The Public’s Bank of China (PBoC) will have end-to-end visibility of the transaction flow and will maintain a register of users and institutions using DC/EP. It will have the ability to decline or confirm a transaction.

But, there is a small glimmer for anonymity. PBoC – in designing DC/EP – formed a system called “loosely coupled account links”. This implied that a transaction can take place between two wallets, without any being associated with a bank account. This leaves room for users to transfer from wallet-to-wallet without revealing transaction details. But at the same time, the PBoC will retain control over the activity of the wallet and, unlike a Blockchain-based crypto system, can easily use the centralized status of DCEP to block or reverse a wallet transaction.

By now, the distinction between a usual cryptocurrency and the DC/EP should be apparent. Not surprisingly, the DC/EP started-off as an ambitious project, but has since entered the conscious of most central banks.

Central Bank Digital Currencies (CBDCs)

Collectively, this trend of central banks working on digital currencies has made the Central Bank Digital Currencies (CBDCs) a common jargon.

Ecuador launched a digital currency project as early as 2014, but the failure to attract users meant that it discontinued in 2016. The Netherlands, similarly, did internal experiments in 2015. In another year, central banks from England, Singapore, Canada, and Estonia also joined the fervour. But the case for digital currencies was weak, still.

The experiments expanded further to Hong Kong, Japan, Sweden, and central banks of many other countries. And today, especially with the averseness to cash amid the pandemic, the outlook and attractiveness of digital currencies have largely improved. LBCOIN (Lithuania), and e-krona (Sweden) are examples of some banks’ fast progressing towards bigger pilots and implementation. Even in the U.S., while the Federal Reserve and several committees downplayed the effect of CBDCs, the Cryptocurrency Act signed in March and the news on the Digital Dollar project reveal the true intentions.

The growing excitement is hard to miss, especially when almost all big central banks and organisations such as IMF, BIS are reporting heavily on CBDCs. In fact, the recent working paper by BIS mentioned that over 80% of the surveyed central banks were by mid-July engaged in “research, experimentation, or development of CBDCs”. To add, 36 central banks have already published work on CBDCs.

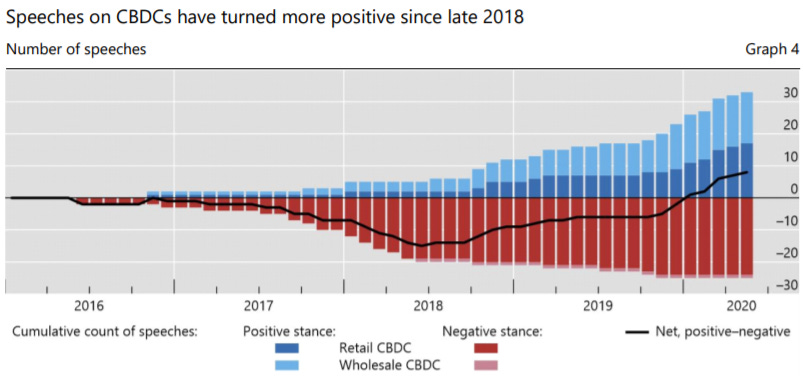

The report by BIS particularly does a great job of highlighting the rising popularity of CBDCs. A graph below shows the increasing inclusion of CBDCs in central bank speeches, as well as the positive turning sentiment towards them.

Source: Bank for International Settlements (BIS)

There are two points of note in the graph:

The trendline for the overall positive stances has turned steep, while for the negative sentiments has turned almost flat. Of course, the lack of visibility into views on CBDCs from many central banks makes this a limited and perhaps incomplete sample, while the subjective assessment of remarks makes it dubious. But the trend does reflect the direction of the flow of sentiments.

Second, the optimism is mainly led by wholesale CBDCs, while the retail CBDCs have been net-negative in sentiments.

For starters, wholesale CBDCs are instruments for settlements between financial institutions. The issuance of CBDCs with these bank-to-bank transfers has been more acceptable for central banks, with the motivations mainly towards payments safety – especially of cross-border transactions, and towards payments and financial stability of the financial institutions.

On the other hand, retail CBDCs are the central bank liabilities for general-purpose use. Similar to the DC/EP experiment in China, retail CBDCs give the public a cash-like claim on the central bank. While they have attracted more attention, the scrutiny and doubts have been bigger as well – especially concerning their relation to the private sector. Saying that, the Bank for International Settlements (BIS) report states that since 2018, the sentiments towards retail CBDCs have turned net positive, with the number of central banks willing to issue a retail CBDC doubling in 2019 – to 20%.

Ecuador, Ukraine, and Uruguay have already completed pilots with their retail CBDC, while six other pilots are in progress. At the same time, multiple banks continue to remain cautious with retail CBDCs. The biggest driver of this trend is the potential improvement in payment safety and robustness, with the domestic payment efficiency and financial stability contributing to the support for retail CBDCs.

What purpose do these CBDCs solve?

Breaking the US’ monetary sovereignty is one part of DC/EP, but for CBDCs in general –the motivations for issuance vary. There are, however, some commonalities associated with most of the research and pilot projects.

Greater visibility over the financial flows through centralized registers that would help counter money laundering and terrorism financing

Establish control over the financial system and capital accounts, while displacing the threats posed by anonymous cryptocurrencies

Improve the effectiveness of monetary policy by strengthening the pass-through of policy rates to bank rates

Safer alternatives for transactions and deposits than those transacted with the bank. For risk-averse households especially, retail CBDCs offer a safer alternative to withdrawing money with backing from the central bank.

Lastly, especially for emerging economies, financial inclusion has seen an important motivator for CBDCs. This is compounded by the fact that people are more likely to hold smartphones than a bank account in several such countries.

The diverse motives also make the use cases equally diverse. For developed nations, the government-to-person payments as an alternative to credit transfers and cheques make CBDCs attractive, while the private sector contemplates the B2B use cases for retail CBDCs. Similarly, for developing nations, countering the large levels of informal activity has been the major focus. India, for example, has been attempting to displace cash over the last four years with little to show after all the efforts. These motives and use cases add complexity to the development of tens of such digital currencies.

This is why, to structure the rhetoric around CBDCs, the central banks of the U.K., Japan, Sweden, Switzerland, U.S. with the European Central Bank (ECB) and Bank for International Settlements (BIS) released a paper last week, setting out the criteria that need to be justified for any central bank to issue a digital currency. The paper states three “core principles” that appear quite wide and grey on the first look:

A central bank should not compromise monetary or financial stability by issuing a CBDC

A CBDC would need to coexist with and complement existing forms of money; and

A CBDC should promote innovation and efficiency

At the center of these principles are the fears that direct central bank transfers may push to disintermediate the banking system, with the move of deposits to CBDCs squeezing the banks’ funding and liquidity. At the same time, the report does well to highlight the potential for this new form of money.

Why suddenly now?

The talk around CBDCs has been ongoing for years now, with mentions of the idea going back even decades. But this year, there has been a spike in the interest from central banks and consumers alike.

Source: Google Search Trends for ‘CBDC’ over last five years

The graph above neatly shows the rising interest in CBDCs. There are a few explanations:

The desire to respond to the dependence on and costs of cash has become greater with COVID-19. This has tilted the interest of central banks earlier sitting in the middle, especially with the global digitisation of commerce and the development of private digital currencies.

The Libra project by Facebook, which aims to work centrally as do CBDCs, made the concept more conscious in the minds of public banks. At the same time, PBoC and central banks in Europe saw this as another US-based payment system and a threat to their influence, which heightened the pace of their efforts towards CBDCs. Interestingly, a draft statement by G7 recently mentioned that they would not accept the launch of Libra before the research is completed on CBDCs.

To add, the experiments by China, Sweden, and other central banks have shown new and emerging use cases for the state-backed digital currencies, which has given more confidence for banks on the sidelines to finally start acting on them.

Lastly, the fear of missing out (FOMO!) is real. We see that on social media, in venture capital, and it seems – at the highest levels of central banks as well. With more central banks jumping on the ship, the ones nearby don’t want to be left behind.

What’s next?

Over the next decade, several countries will have almost certainly adopted CBDCs to some extent. It will differ, however, how the rules for processing, conversion, and exchange are laid down, the purpose for adoption or the use cases at varying development stages, the role of commercial banks in the process, and the acceptance of the private sector within the eco-system.

For one, as the BIS report also states, countries with better digital infrastructures w.r.t. online and mobile use will be able to distribute the currency better to the public and see better acceptance. Similarly, countries with a high level of government effectiveness and efficiency are more likely to launch their CBDC projects. This would be a hurdle to most free-market developing countries, which theoretically see lower government effectiveness.

Moreover, the risks to commercial banks - as private accounts with central banks become viable - will potentially introduce a conflict of interest for the governments, as well as make the distribution challenging in countries with no alternatives.

Besides, if CBDCs are pushed by the governments, we can expect the efforts to replace cash gain incredible pace. This is supported by the recent report by dGen, a European think tank, that expects CBDCs to entirely replace the fiat currency in three to five countries by the end of the decade. Lastly, and importantly, the simple wallet-to-wallet transfers would make cross-border flows, incl. the cross-border settlements and the remittances transfers, lower cost and less complicated. This can potentially improve trade between countries and support efforts towards globalization and trade openness.

While China started the experiments with the purpose of domestic control and global influence, the efforts have changed how CBDCs operate and exist in the minds of central banks. With the pandemic scaling everything digital and the payment systems becoming as dynamic as they are, the developments in this area might be the most significant. Perhaps, changing forever the nature of fiat as we know it today.

Other interesting reads on the topic:

On the Flipside of China’s central bank digital currency by Australian Strategic Policy Initiative

On the foundational principles and core features of CBDCs by central banks, BIS, and ECB

On the Geopolitical Ramifications of a Major Digital Currency by dGen

If you have any views or feedback to share, feel free to add a response below or to share your thoughts with me over Linkedin. In case you feel your friends or family would be interested in reading about fintech or economics, feel free to share the blog with them as well. See you in a week or two!