Account Aggregators and the Payments Possibilities (#39)

How AAs can help reward programs, credit cards, and other parts of payments

Welcome to the 39th issue of the Unit Economics. Today’s article discusses the promising Account Aggregator (AA) system and hypothesises how Indian payments co’s can benefit from it. Jump in!

The last fortnight has been immense for the Indian Fintech ecosystem.

First, Prosus, a Dutch tech giant – which also operates PayU, announced the acquisition of BillDesk for $4.7 Bn. If the acquisition does go through, it will be - by some distance - the biggest for any Indian Fintech company and rank amongst the top ten in the world for the industry. It will also give PayU + BillDesk more than an estimated >2/3rd of the payment processing share in the country.

Second, the go-live of the Account Aggregator (AA) ecosystem has introduced murmurs of a UPI-like moment for Indian Open Banking. The merit of the AA framework is easy to understand. But the extent of possibilities that it promises can be quite tough to grasp.

For this write-up, given the excitement around the second milestone, I deliberate on the AA system launch and its likely impact on payments.

But before, what is the Account Aggregator (AA) Framework?

What problem does it intend to solve?

Traditionally, an individual’s financial data has been held and regulated disjointedly by multiple institutions – central bank, insurance authority, securities board, pension funds. This has led to the development of multiple standards for processing user applications and has made transferring the data from one financial institution to another an operationally challenging effort - filled with physical paperwork and asynchronous approvals.

The inefficient processes have pushed the Fintech companies to choose between (1) utilising the existing user information from third-party financial institutions but making the onboarding complicated by doing so, and (2) establishing user’s profile through proprietary methods but achieving relatively inaccurate results as a consequence.

The outcome of such challenges in accessing and sharing the financial data are two-fold: (1) inconsistency in the processing of user profiles across companies, and (2) the financial exclusion of many in the country.

How does the AA framework solve this problem?

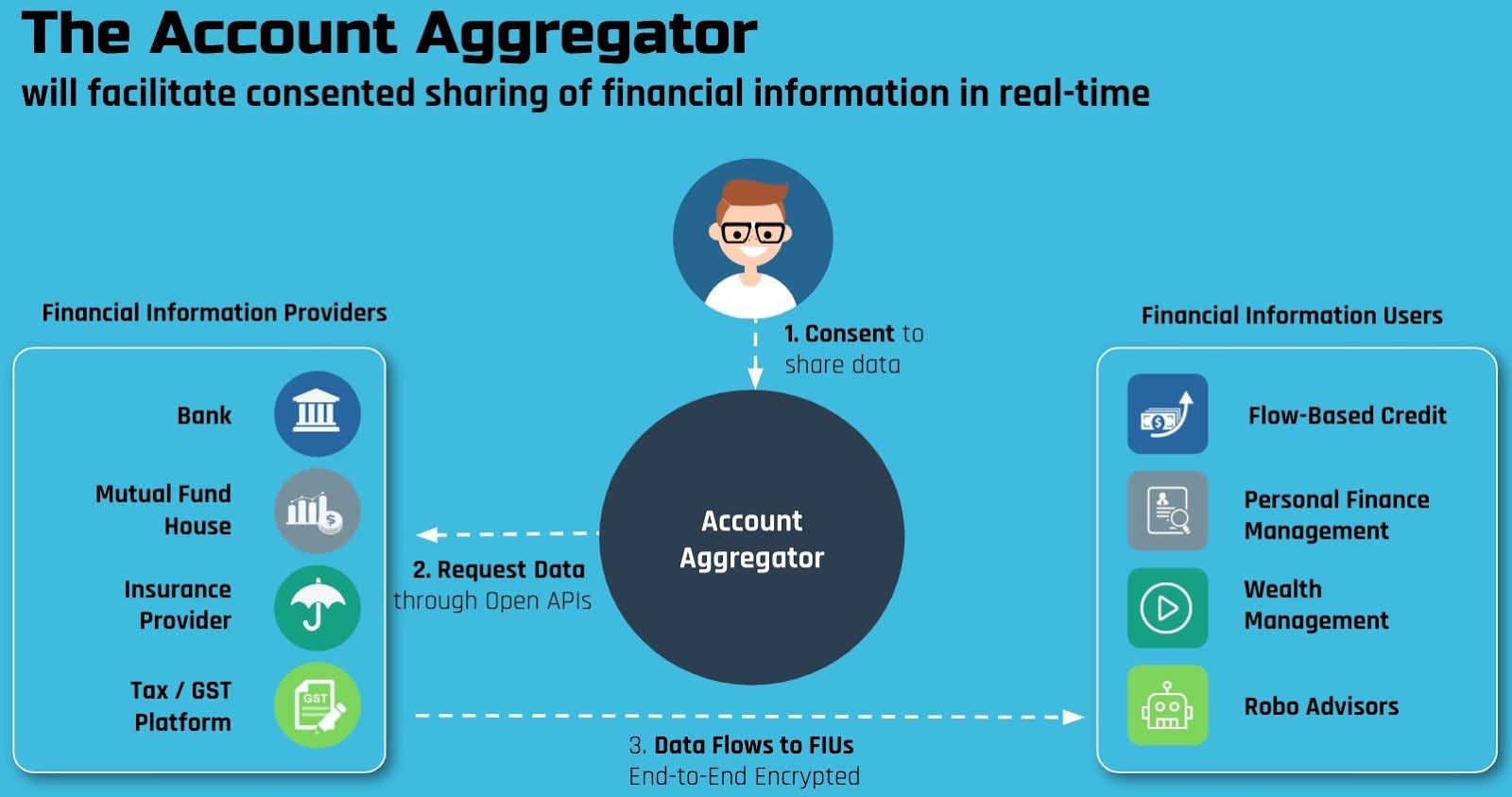

The framework defines an architecture (image below) with multiple participants, who will combine to digitally enable consent-driven sharing of data from one or multiple financial entities to another in real-time. Digital, consent, real-time – each is a crucial feature that makes the jump from the traditional methods, of data sharing by uploading or by revealing account login information, to the new method substantial.

Further, understanding the roles of the four participants helps get a better sense of how the system would operate:

Financial Information Providers (FIPs): institutions such as banks, mutual and pension funds, etc. that are the source of personal or business data. Account Aggregators (AA) will share this data with the FIUs (below) on the user’s consent.

Financial Information Users (FIUs): institutions that will receive the digitally signed data from FIPs through AAs. The FIUs can then use the data for purposes declared in the data-sharing agreement.

Account Aggregators (AAs): RBI licensed entities that will act as conduits between the FIPs and FIUs by providing a digital platform for sharing the financial information. The AAs will, however, be data blind. They will not see or process the data – but will only facilitate the exchange. This description cleanly demarcates the data-related responsibility by stating which participant can produce (FIP), transfer (AA), or process (FIU) the data.

Technical Service Providers (TSPs): companies that will help FIUs and FIPs deliver the required capabilities to facilitate usage of AA system, including but not limited to product design of FIU applications, and developing underwriting, wealth management, or personal finance management use cases.

Given the high number of use cases, the possibility of significant volumes and revenues for participants, and the likely improvement in quality of user assessment, there are already 15 institutions (likely more that are yet to be updated in the list) in various stages of FIP/FIU implementation.

But following the developments, one would notice that a large part of the narrative has centered around lending. And there is good reason for lending companies to be excited about the AA architecture, especially with the requirement of making a yes or no decision in the credit journey – a step that is not always present in the payments, investment, or insurance flows. The user’s balance and transaction data, undoubtedly, will be of great help to lenders here. With the added information, we should expect lending FIUs to build more elaborate user profiles, process applications quicker, onboard a higher proportion of applicants, and achieve lower NPAs – each of which would be a result worth appreciating.

But for our purpose, let’s go deeper into where payments companies can benefit.

Payments and Account Aggregators

Now, there is not always a clear distinction between payments and lending. We know that credit cards and BNPL applications are debt instruments, even if they differ from traditional personal loans. So, many of the expected improvements in lending are likely to accompany the debt payment instruments. But there are sufficient payments-only use cases that will benefit from the AA framework.

Below, I explore both types - debit and credit - of use cases for payments and in doing so, I occasionally use lessons from Plaid – a company that has operated much like an Account Aggregator for over 300 Mn bank accounts and that powers some of the biggest names in Fintech (Venmo, Chime, Robinhood among others).

Personalised Nudges – Link Rewards to Potential

Today, rewards such as cashbacks and discount vouchers are commonly accepted currencies for payments applications. You are likely to come across few acquisition strategies that do not promise such benefits. But there is a problem here. The onboarding journeys of debit payments products focus little on understanding the user’s financial profile. This means that transaction-based rewards are almost equally distributed across the activated users – despite the differences in potential value that users will add to your business. This is far from ideal.

With bank balances, transaction, and investment data, the debit applications (wallets, UPI) will benefit from building estimates of potential lifetime value that a user can give to your business at the time of onboarding. The estimates should then be used to divide users into different groups (based on potential LTV), and to incur acquisition costs on rewards such that the costs align more linearly with the potential business value of the user.

The core idea here is to use the AA data to build reward engines at a more micro level and to build offers for different sets of users based on their transaction potential. With this, payments products will give themselves a higher chance to attain positive unit economics by extracting greater value for the same acquisition cost.

International Payments – Automate to Initiate Transfer

Outward remittance is an unsolved problem in the country, with little support from even the UPI system. The process of initiating a transaction requires manually entering your bank account details or card numbers, routing information, and incurring high fees.

Much like Plaid has done with Paysend and Wise, the AA framework will allow users to link their bank accounts to pre-fill required account details, reducing the time to initiate the transfer by over half (the drop was 80% for Paysend). In addition, the user's remittance and transaction data can be used to inform the user of their previous financial decisions and help prevent overspending and overdrafts – offering a higher conversion and better user experience.

Overdrafts, Failed Payments, and Fraud

Two of the key reasons for failures in bank transfers are overdrafts and mistakes in manual entry of account information. For UPI transfers, this problem is resolved by showing balances and wrapping all the account information into a simple VPA. However, for users that pay through Net Banking – the absence of a UPI ID still invokes a lengthy process.

Similar to how the AA framework would solve for international payments, the two errors can be bought down by pre-filling the required account details and by disallowing initiation for overdraft payments. Further, the required authentication for AA data makes the process less prone to fraud, as opposed to entering the account details manually.

Such promises are validated by the Wave Financial case study. By linking bank accounts through Plaid, Wave was able to lower fraud by 60% (with account authentication) and reduce the likelihood of failed payments due to mistake in entries by 5.6 times.

Credit Cards – A New Lifeline?

Indians hold over 400 Mn savings and current accounts, over 830 Mn debit cards, but only 58-60 Mn credit cards today. And even then, there would not be more than 40 million unique credit card holders, i.e., a figure less than 10% of the population with bank accounts. Now, compare that to over 1.5 Bn credit cards in the USA alone.

Why does the difference exist? The answer lies in (1) the lack of accessibility of credit cards, with the requirement to prove some formal credit history during the application, and (2) the resultant perception of the credits cards as a luxury-only product.

The growth in the number of bank accounts and the ability to leverage the account data should help bridge the credit card gap over the next few years. Much on the lines of the last article, the AA framework would help companies utilise the transaction and the balance + savings information as alternative data to allow access to credit products. Maybe this will be the much-needed push for credit cards in the country. Remember that there are still no direct substitutes to credit cards - with definite spend-linked rewards as the value proposition - amongst payments products. So, there is ample potential.

Onboarding – Simpler and More Effective

The KYC requirements make the onboarding journeys painful enough. But the need to assess user’s financial information only adds to the pain for credit payments applications, with extra fields on income and other personal information.

With the AA login, the users will instead link their salary and investment accounts with a few clicks. This will help FIUs not only lower the onboarding time but also get a more accurate picture of the user's financial profile. Result: onboarding becomes lighter with fewer input fields, and everyone wins.

What does all this mean?

Understand that for both users and financial institutions, the core shift will be from asynchronous access of the distributed user information towards real-time access to a single and more elaborate profile.

With the account aggregator as the gatekeeper of the income, credit, and investment history of the user, this single profile will open doors for the user to access more diverse financial services. Moreover, the availability of user data will lower the operational efforts for the Financial Information Users (FIUs), allowing them to offer their services at lower costs and to more people.

For payments, we see that this can translate into differentiated rewards, targeted merchant offers, better unit economics, fewer payment failures and frauds, and smoother onboarding and payments initiation. Equally, the ability to understand the user’s financial profile will aid the payments companies in cross-selling the relevant higher-margin financial products, even without owning the entire transaction or account data of users and merchants. Saying this, this is still day one for the Account Aggregator (AA) system and there are likely to be more niche use cases for payments to look forward to. We will, I believe, revisit this topic quite often in the next few years.

If you have any thoughts on the topic, write back to me on Linkedin or drop a comment below. In case you feel your friends or family would be interested in reading about payments, feel free to share the blog with them as well. See you in a couple of weeks!