The State of Point-of-Sale Payments (#34)

The shift in how customers and merchant interact at the point-of-sale

Welcome to the 34th issue of the Unit Economics. The write-up today talks about the last decade of shift in the in-store payments behaviour and wonders how it can change in the next. Read up!

The talk around e-commerce can sometimes mask the changes in offline retail. Despite the huge dent that e-commerce payments have made, roughly six out of seven transactions continue to be in brick-and-mortar or mom-and-pop stores. The ratio, as you would guess, turns even more favorable for offline purchases in the relatively less developed regions and for more experiential products. Any change then that upends how offline commerce is conducted is hard to ignore for its magnitude and should have tremendous ripple effects.

This is obvious when we look at the shifts over the last two decades. From the 2000s, we have seen payments acceptance move quietly away from the traditional cash registers and heavy POS machines to the smaller, mobile, and cloud POS terminals. When combined with lower settlement times, lower cost of acceptance, improved business management with POS systems, and a higher number of payment methods – we can more easily grasp the degree of change.

For the customers, as we all would have experienced, the physical wallets have turned into card holders and the money has instead moved to digital wallets or stayed put in banks, all while adding more convenience to our buying experiences. The types of point-of-sale credit have similarly expanded from credit cards to a set of wider and inclusive credit payments (E.g., EMIs, BNPL).

These and many other shifts underline the last decade for POS payments. To understand the present state of POS payments better, let us think of a simple payments value chain for offline stores.

Step 1: Customer selects the product(s)

Step 2: Customer selects the payment method

Step 3: Merchant accepts the method and the payment

Step 1: Selecting the Product(s)

This might not naturally indicate a direct connection, yet the selection of products in the cart is more tied to payments today than ever before. The Think with Google consumer insights helps us understand how the omnichannel experience, from discovery to the selection, is driving the consumers’ in-store purchases.

A global survey, conducted in Feb-19, indicates that 74% of all in-store shoppers search online before going to the stop to shop

Moreover, 59% of shoppers use Google to research a purchase that they plan to make in-store or online

Lastly, more than 50% of the surveyed shoppers use Google to discover or find a new brand

In context, these statistics simply imply that following a non-linear path, the customers today discover, consider, or make the decision to buy a product both offline and online (social media, merchant website) in any order. The additional points of information allow customers to make more informed decisions about pricing & merchant before they end up selecting their end cart, leaving less room for impulse purchases.

Think of, for instance, how often we evaluate payment rewards and product prices when scouting restaurants on Zomato or Dineout, or when leaving home to purchase shoes or clothes. The discounts, cashbacks on memberships and particular payment methods are unknowingly driving the product selection for us digital-first customers in many such cases. A direct implication of this is that we are today discovering brands and buying from merchants that we would likely not have heard of ten years ago, making loyalty a tougher buy for the merchants.

The next part on how POS payments have shifted at selection is related to a new method of retail shopping: Click and Collect. Funnily also known as BOPIS (buy online, pick-up in store), the click and collect model allows shoppers to make purchases online (including selection and payment), and collect the order from a physical location, including store, warehouses, designated lockers. This POS trend has seriously picked up during the pandemic, with an e-commerce platform – Kibo Commerce – seeing 44% of all purchases through click & collect and volumes through the method grow at over 500%! Customers benefit from the speed of collection and the cost savings on delivery, while the merchants find the ease of launching the method, the potential to deliver an in-store experience, and lower reliance on third-parties comfortable through Click and Collect.

Step 2: Selecting the Payment Method

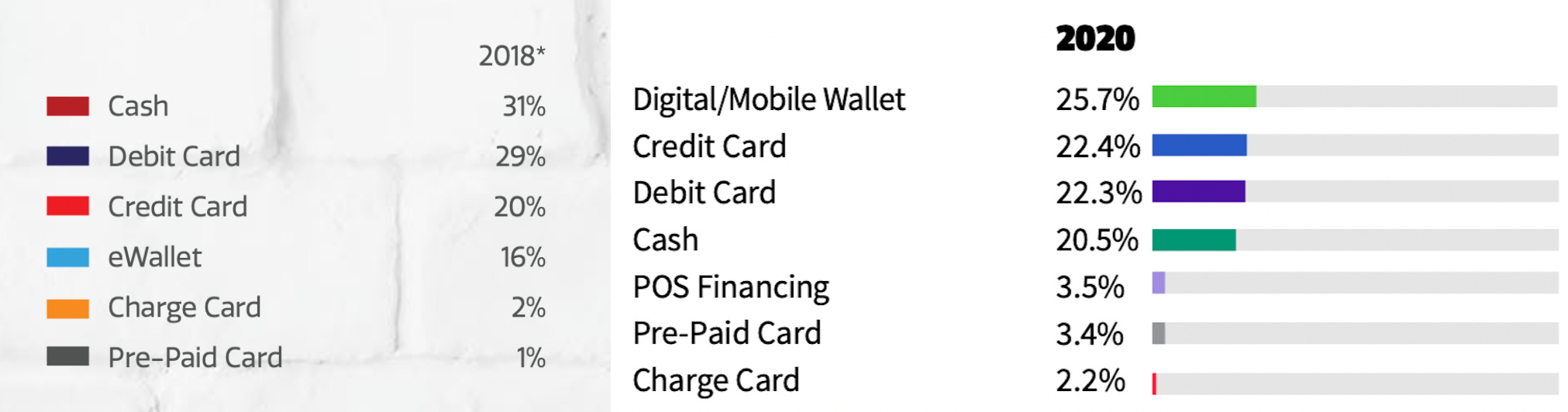

Travel back to the 2000s, and you are likely picking out cash or a credit/debit card for an in-store payment with little thought for any other method. But with the pace of payments innovation, the last decade has allowed customers a much broader set of options, including digital wallets with QR and contactless (Apple Pay, Paytm, Venmo, etc.), virtual tokenized cards, BNPL and other installment options, A2A transfers (UPI, Pix, etc.), and, at a lower scale, blockchain-based CBCDs and cryptocurrencies.

We see that cash and cards continue to make up a majority of the POS payment volumes, but it is remarkable to think that digital wallets (helped by QR codes) make up almost a quarter of these volumes from being non-existent a decade ago. Not surprisingly, some of the most popular payments companies have leveraged wallets in this period to gain volumes: Alipay, Paytm, WeChat Pay, Apple Pay, Samsung Pay, among others. Moreover, the introduction of CBDCs, which would act as direct substitutes of cash, could take physical cash in the same direction as physical wallets over the next decade.

For cards, while the form factor appears the same, the utility and rewards are fast transforming to adjust to the challenges post by alternate payment methods.

Research suggests that the annualized growth of contactless card payments (NFC-enabled, also known as tap-and-go) would be ~20.3% for the 2021-28 period, higher than the expected growth of POS commerce. The expectations are derived from how contactless cards lower the friction at checkout and generate a higher approval (and stickiness) for customers that use them.

Within the contactless cards, a significant push is predicted from cards that offer biometric authentication – a method greatly accepted as more secure than most others available at POS, and a quality that – with the rising fraud – will be a great pull for biometric cards.

Lastly, to adapt to the mobile payments trend, card issuers are diversifying to virtual cards with the added security of tokenization, lowering the issuance complexity that comes with physical cards. Juniper expects virtual card transactions to increase by 370% over the next five years.

The three trends along with high distribution-focus and the rewards of credit cards are likely to keep cards relevant at merchant POS for at least the next decade, but a standard card then might look completely different from how it does today.

Next, powered by the Gen-Z and the younger millennials and with the convenience of digital wallets & the features of credit cards, the Buy Now Pay Later payments are catching up to almost all sizes and industries for payments. Expected to be the fastest-growing payment method, BNPL is being experimented with through white-label solutions from merchants, who are launching installment payments of their own, and through large-scale ticket sizes (flights, hotels, electronics, etc.). Additionally, given its popularity, BNPL is increasingly being tied as an additional feature for payment methods such as cards and wallets.

In the same vein and lying beneath much of the payment methods discussed earlier, payment providers are gradually moving towards real-time account-to-account transfers, removing the delay in settlements and the costs that arose from payment processors as the middlemen. UPI (India), Pix (Brazil), and New Payments Platform (NPP) are three of the more successful RTP systems that have helped businesses lower their costs. To add, real-time payments are being enabled under almost all payment methods today (Bullet – BNPL on UPI; Visa Direct – debit cards on real-time payments, among others), signaling high utility.

Finally, not as common, but wearables appear promising to become the next popular method for POS payments. Apple Watch, for instance, popularly offers the ability to add Apple Pay to the watch and pay using NFC in stores through a simple tap. The promise of adding payments to an everyday omnipresent object has also pushed banks in India such as Axis and SBI to launch wearables devices and add payments functionality to popular watches. To add, the innovators in the field have gradually expanded the payments offerings from watches to wristbands, fitness trackers, and rings over the last few years and the market for wearable payments is expected to showcase a significant 27.2% growth over the next six, according to KBV Research.

Step 3: Merchant accepts the Method and the Payment

For merchants, the costs and the possibility of increased sales have long defined their choices of payment options to provide. This is one of the reasons why BNPL, which promises better conversions, is popular for merchants despite higher average fees than other methods. But it was ten years ago that the standardization of much of the POS acceptance and the expansion of payment methods introduced the innovation in both hardware and software that we see at POS terminals.

Let us go back a little in time. In the 1970s and 80s, the technology for acceptance was driven largely around cash (patent for POS system built for McDonald’s in 1974) and computers had allowed innovations in graphical interfaces for merchants that showed items purchased and calculation for bills.

{kind=link}

The 1990s then introduced credit cards and personal computers to the masses, forcing POS systems to become more flexible. This led to the development of more sophisticated order management systems for restaurants, airports, and retail merchants.

Fast forward to the 2010s, and the number of payment methods and the quality of software development has jumped eons ahead. The POS terminals, in this period, have replaced desktop POS systems with mobile or mPOS and all-in-one POS systems (work both on computer and mobile). This has allowed acceptance to become untethered from the checkout counter and to be carried out at dinner tables and shop floor.

The newer POS software, unlike the 1990s, is also often cloud-based (also called softPOS) – allowing merchants to access data from any device. Moreover, mPOS terminals have expanded in the range of devices – mobile, tablets – and enable integration with multiple hardware peripherals such as scanners, rather than a simple card reader and with business applications such as billing systems to provide complete set of business services. It should come as little surprise then that mPOS terminals are expected to grow at a healthy 18% over the next seven years.

More interestingly, the modern terminals have capabilities that stretch far beyond payments acceptance. The earlier systems comfortably offered inventory management and reporting, with information on the availability of stock, pricing, markup available, daily sales reports, among other basic business details. Today’s innovations, however, have improved the ability of POS systems to provide customer relationship management (CRM) tools that allow merchants to learn about user behavior, give personalized recommendations, design loyalty programs, and offer custom-made payment solutions – including pay later. The addition of features in POS systems has become similar to any of the application updates we encounter, and the innovations have allowed merchants of all sizes to select devices based on their cost appetite.

This brings me to the next point. The lower cost and the increase in functionalities of POS have meant that even the most micro-sized business can buy such devices for accepting cards and digital payments, and manage their employee performance, sales, and customers along with it - without wondering about the costs. This is especially notable in how UPI has been adopted by tens of millions of small businesses and mom-and-pop stores due to the low cost of accepting through a simple static QR code and of managing accounts using a smartphone application. We can expect greater innovation particularly in the area of low-cost acceptance, with segments such as offline-to-offline largely untouched.

Finally, the crowding of the payment methods and the omnichannel acceptance are pushing competition for acceptance at merchant POS, providing merchants an opportunity to push payment choices that benefit their interests and push distribution for certain methods. This is similar to what we are seeing in packed online checkout space – the shelf space can only fit so much, and the payment providers need to pay up to get a place.

Thoughts on the Future of POS Payments

The omnichannel decision making, click and collect model, instalment and blockchain-based payments, new card and wearable payments technology, crowded payment options, cloud-based acceptance, and competition on value-added services for POS devices are all trends that I expect will continue to further improve the customer & merchant POS payments experience.

But what else do we imagine the POS future would like it in ten years? We are getting some hints already.

Amazon’s audacious Just Walk Out Shopping at Amazon Go allows customers in over 20 stores to identify themselves, and simply pick up and leave with any products on the shelves. The amount, based on the identification and products picked, gets automatically deducted from your account. Amazon has even combined the experiment with Amazon One technology, which reads the palm of the customer to identify Amazon profile and accept payments.

VTB Bank (Russia) and Visa are testing ‘Pay by Glance’ in restaurants that allow customers to pay within one second by looking at the camera, assuming they have registered on the payment application and linked their cards to it.

Similar experiments had been made by Nets in 2019, which had tested Pay by Face wherein facial recognition had been used to process payments. Nestle (Spain) and Shinhan Card (South Korea), among others, have previously attempted Pay by Face as well.

A couple of things become apparent from these examples: 1) customer convenience, as always, is driving payments technology at POS, and 2) biometrics seem the most popular choice for payments – assuming that it would make for the most unique, secure, and fastest method of payment, while also obviating the need to carry any physical object (including a mobile phone).

The concerns with privacy and approval from customers remain for these biometric technologies to gain large-scale acceptance. Yet, once the utility of a payment method is justified, consumers – as often – would revolt first and likely accept the method for its benefits in little time.

As for the merchants, the development of the POS machines into business tools is likely to make them more data-rich. This will allow the more large scale merchants to offer services at checkout that we presently associate with only online checkouts, including suggesting add-ons based on products in the cart, displaying lists of offers on different payment methods to the customer to offer easier selection, and personalising communication based on past purchase history of new additions to the store or of price drops.

Lastly, watch out for the expansion of online-only payment providers in the POS payments chain, because offline payments are here to stay!

If you have any views or feedback to share, feel free to add a response below or to share your thoughts with me over Linkedin. In case you feel your friends or family would be interested in reading about payments, feel free to share the blog with them as well. See you in a couple of weeks!