The New Era of Credit Cards (#40)

Disruptions in designs, rewards, repayments and every other part of the credit card experience

Welcome to the 40th issue of Unit Economics. It’s good to get back to writing after a small break. For today’s issue, I talk about the re-emergence of credit card innovation after decades of relative inactivity. Dive in!

Seventy years is a long time. For most technologies and products, it is sufficient to force drastic change or to process a collapse. But this is not true of credit cards, which have surprisingly handled the time with minimal changes to the core – and yet achieved much success.

With rather modest beginnings as charge cards in the 1950s, the cards were then a privilege meant to be used in popular restaurants and department stores. In the 60s and 70s, as the card networks became sophisticated, and the banks saw the obvious merit in the convenience and business model of revolving credit – the plastic was pushed as a financial product for all household purchases. The popularity attracted mischief and gave way to more secure card encryption, moving gradually away from the magnetic stripes in the 90s. In a way, such improvements in card security were among the few noticeable developments for credit cards, and they seemed forced largely due to the advancements in fraud practices.

For the few card networks, there was – for this long while – little incentive to re-think the credit cards. In the 90s, there continued significant growth in merchant and issuer networks for the likes of Visa and Mastercard. And by 2001, in the USA, an average family had annual credit card debt of ~$4,126 – accumulating to $692 Bn in debt at an aggregate level. With this success of credit cards, more time was likely spent discussing regulations around interchange than on technology.

By the mid-2000s, when the interest in online payments was quite nascent, there were still no payment methods that could compete with the convenience of easy-to-swipe credit cards. Cash and cheque – still popular – stayed painful for merchants. And net banking was a luxury that solved for large money transfers but could hardly compete on payments with cards. But as the world woke up to the newer digital mode of payments with the entry of PayPal, Alipay, and the like – credit card payments finally had new challengers, and not just the old guards, to deal with.

Now, fast forward to today. Online, credit cards struggle against BNPL, A2A transfers, mobile wallets, direct debits, and the many new digital payment methods for market share. At the point-of-sale, the agony is similar against mobile wallets, POS financing options, and bank transfers that happen in real-time. What has all this competition done? It has forced card networks and issuers to re-imagine the sturdy-old credit cards.

So, what is changing?

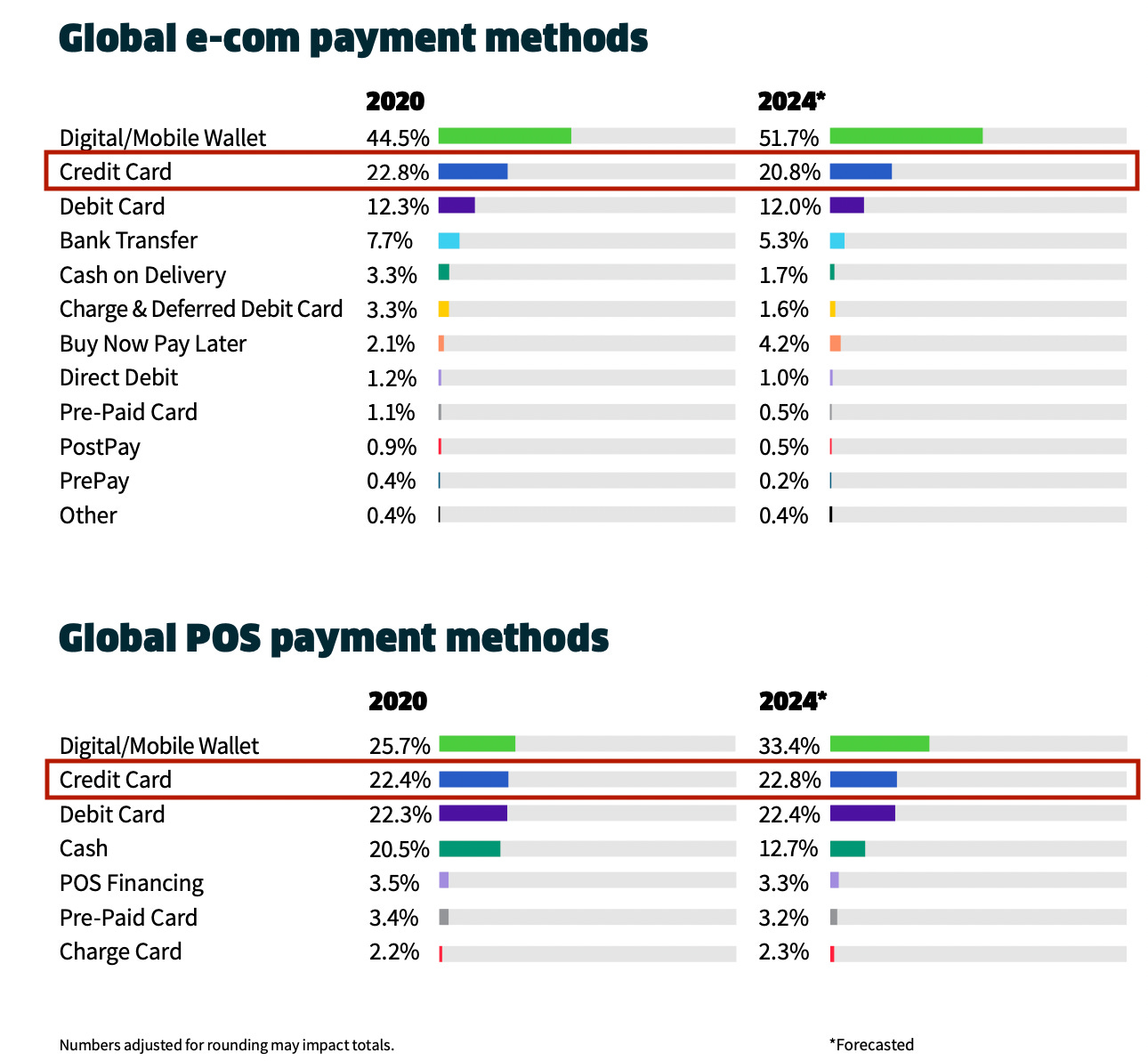

For one, the consumer preferences. The share of credit card spend in e-commerce is expected to fall, given the present trendline, and to remain stagnant at the point-of-sale (POS). Both are not particularly great news for credit cards.

One bit of good news is that credit cards will still likely remain one of the top three payment methods of choice. But for how long? Depends on how fast they adapt to the new expectations. Survival requires offering the same quality of features and level of convenience that other digital methods do. Let us think a little more deeply about what that would mean for credit cards.

1) Accessibility: Everyone wants credit

People might not need it, but they love to use credit for travel, entertainment, hotels, and roughly all other spendings. And credit cards allow them to do that with a swipe or a tap.

Yet, the issuers have not made it easy for people to access credit cards. Long onboardings, strict credit history checks, and the wait for physical delivery of cards – little was done for a long time to make cards accessible.

This is changing, however, as (1) incumbents struggle for acquisition and adopt more flexible approval processes, and (2) Fintech companies use alternative data to evaluate credit seekers (had written earlier on how AA’s or payments co’s can do their bit).

Two good examples of companies that have made credit cards popularly accessible are Petal (100K+ approved users) and Slice (3 Mn+ users). Petal uses banking info to evaluate those without credit history and such users make up 70% of its entire base. Slice, on the other hand, uses user-declared data and certain alternate sources to onboard users. And both companies have, in a short time, developed a proven record of performance and quality risk assessment. There are others of course, such as GalaxyCard, that are similarly solving for credit card access in different ways.

Given the need, in this decade, alternative data and experiments on ways to evaluate creditworthiness will remain important for the popularity and accessibility of credit cards this decade.

2) Design: Personalisation is key

To attract users that face multiple options for payment methods, it is important to constantly deliver experiences that wow them. For credit cards, if the onboarding does not do that, the design of the physical card offers another opportunity. But the card is more complicated to design than you’d think. For issuers, it involves deciding on the card material, weight of the card, colors, patterns, images, custom names, the position of logos, stripes, text, and card information all within the confines of a small rectangle – and to make it stand out.

Examples can help validate how quickly the design has evolved as a key credit card proposition, signalling a shift from the standard plastic cards from not too long ago.

Monzo has popularly used the bright design of its bank cards as a marketing tool

Card networks have begun offering numberless cards for increased security, with the likes of Banco Santander and Fampay adopting the designs

RHB Bank (Malaysia), DBS Bank, and the card networks have attempted to replace plastic with more eco-friendly and recyclable materials – in line with the values that many subscribe to today

Mastercard has introduced the True Name initiative targeted towards Transgender people, who can now add their chosen name, instead of legal name, on the cards – making the card programs more inclusive

The likes of Curve and OneCard have successfully used Metal to build premium brand perception

The examples offer a view of how the design can help differentiate cards from other non-physical forms of payment methods. Also, note how quickly issuers have challenged the status quo for card design in the last few years. If the thought of designing a credit card’s appearance interests you, you might want to spend some time playing around with the Visa Card Designer tool.

3) Rewards: Give people choices

Consumers demand rewards that are simple to earn and redeem, relevant to their wants, and evolve with their requirements (wrote on rewards here). Today, this should translate to rewards that adapt to an individual’s spend behavior, that do away with complicated points-to-currency calculations, or ones that offer more flexibility than the usual goods-in-the-catalog redemption that banks have used for decades.

For credit cards, the reward structure thus shifted focus towards direct cashbacks, rewards on services and trends such as crypto, and reward tiers based on spend behavior. This is an obvious shift from a static to a more fluid and adaptive reward program, where the user has the choice to redeem when he wants, what he wants, and where he wants. And the more choice a user gets, the better the value proposition is of the card.

4) Payments: Remove all friction

Payments innovation continuously focuses on one area: minimizing friction at the point of purchase. Swiping a card is easy enough. But in the last decade, cards have evolved to make payments completely contactless with the NFC technology and allowed cardholders to pay simply by tapping. This technology is today allowing two big shifts:

Cardholders do not require physical cards to make payments and can instead use virtual cards since mobile phones support the NFC capability (E.g. Apple Pay, Samsung Pay, etc.), and

The merchants can accept card payments through soft POS machines, i.e., their mobile phones, with NFC – bringing the entire card payment experience to the mobile phone.

Online, the friction is handled through an ability to store Card-on-File for aggregators and merchants. Card-on-File absolves the need for the user to enter the 16-digits or the expiry for each separate transaction. Subscriptions or recurring payments, one-click checkout, and tokenization are all steps in the same direction for cards.

But what does the future hold? The need is to deliver a frictionless experience while maintaining the highest security standards. At the point of sale, this is achieved through real-time biometric authentication over card payments, or tokenization through mobile or other wearables. For e-commerce, Web3 with the browser-based wallets might be showing the window to the future, where one parent login and transaction consent is sufficient to send money to any online merchant.

5) Repayments: No hidden costs

The traditional credit card model incentivises that a segment of users revolves, which then subsidizes the rewards and services for transactors. The costs of overdrafts or late payments have not exactly been transparent either, and led to a trust deficit for millions of credit seekers over decades.

But for the new-age card issuers, this was an opportunity to re-imagine the repayment journey. Following the popularity of BNPL, companies such as Uni and Slice have introduced features to split card repayments into three or four equal payments. Additionally, these companies stress the no-hidden-fees proposition to stand away from the frills of credit cards. Many others have tried to fill the gaps by making tracking and payments of credit card bills easier (CRED, Paytm, etc.) or by offering the e-NACH facility to auto-debit credit bills. Some go one step ahead to reward timely payments through credit builder programs that help users increase their credit scores (Chime, Apple, Petal, etc.) - a great tool for user acquisition and engagement.

The credit builder programs, transparent costs, and flexibility in repayments all signal a move towards more cardholder-friendly behavior for repayments – a trend reversal from the traditional credit card incentive structure. We can expect this area to see more innovation as card issuers attempt to portray themselves as the least of the evils.

6) Card Controls: Mobile-first management

The user experience of a payments product extends to an individual’s ability to control their own experience. The popular PFM features fulfil this very need today.

For card issuers, the experiments have led to breaking down the controls into levers that users can push as and when they like. These include controls for spending limits, time-based or location-based restrictions, merchant hot-listing, channel and transaction type controls, freezing usage, and insights on transactions (e.g. carbon emission stats based on spend behavior). We are in the initial days of mobile card controls today, especially with how exact the controls seem at the point of issuance. Over time, the controls should be enhanced merely with software updates for cardholders and be offered in tiers as additional services for a subscription fee.

Final Few Thoughts on Credit Cards

For a seventy-year-old product, the last few years have been unusually active and innovative. With the possibilities to redesign each part of the credit card life cycle and a proven track record of the card business model, it is not tough to understand why so many startups are suddenly getting into the business of issuing cards.

There is little doubt that the growth in real-time A2A payments (UPI, Pix, etc.) and wallets will continue. But understand that the pie is large enough to accommodate a new stage of adoption for credit cards. Today, the value of credit cards is most validated by the increasing pace of bank partnerships with co-brand issuers such as Paytm, Amazon, Flipkart, etc., and the spurt in the issuance of corporate cards to millions of SMEs and large businesses.

As success stories of more challenger issuers come out, and the designs and proposition of cards improve, we can be hopeful that credit cards will expand their presence and become a household financial product for the Gen-Z’s and newer generations alike.

If you have any views or feedback to share on the topic, feel free to add a response below or to share your thoughts with me over Linkedin. In case you feel your friends or family would be interested in reading about payments, feel free to share the blog with them as well. See you in a couple of weeks!